THE COMPUTE CAPACITY BOTTLENECK $GOOGL just admitted Google Cloud is leaving revenue on the table because it cannot build capacity fast enough with shifts the bottleneck to companies with the power, real estate & operational scale to deploy AI compute: 1. $NBIS building the AI-native cloud layer through vertically integrated GPU clusters & software optimized for training + inference. $NVDA just wrote wrote a $2B check & Nebius now has a $46B contracted backlog, anchored by ~$19B $MSFT deal & ~$27B Meta partnership through 2032. 2. $IREN building the renewable-powered AI compute layer by turning low-cost power into GPU cloud capacity. The pivot to AI cloud is now backed by a ~$10B $MSFT contract, 2.9 GW of grid-connected power expanding to 4.5 GW+ & targeted 140K GPU buildout that could drive $3.4B of ARR by year-end 2026. 3. $DOCN building the agentic inference cloud layer for developers & long-tail AI workloads. AI customer ARR is up 150% YoY to $120M, over 70% comes from inference services & $1M+ customer ARR is up 123% to $133M. 4. $CRWV building the dedicated AI cloud platform for frontier model developers. The company has ~$67B of contracted revenue backlog (nearly $88B including Anthropic) with major commitments from OpenAI & Meta. 5. $CIFR building the Google-backed AI data center layer through contracted power & hyperscale leases. Barber Lake has 300 MW fully contracted with Fluidstack (Google backstops $1.4B with a ~5% equity stake) and AWS signed a separate $5.5B 15-year deal for another 300 MW of capacity. 6. $WULF building the power-backed AI compute layer through long-term data center leases. Lake Mariner has 360 MW tied to Fluidstack backed by a $3.2B Google guarantee & new Abernathy JV adds 168 MW over 25 years representing $9.5B in contracted revenue with $1.3B of Google lease support. 7. $APLD building the purpose-built AI data center layer through its Polaris Forge 1 campus in North Dakota. The full 400 MW critical IT load is contracted to CoreWeave under ~15-year leases worth ~$11B in expected revenue with first 100 MW delivered in Q4 2025 & another 300 MW targeted through 2027.

)](https://www.asme.org/getmedia/02a1e495-6db6-4069-848f-b128f357f5e0/0121_infographic-shifting-sources-for-electric-generation.jpg?ext=.jpg&height=4020&width=954)

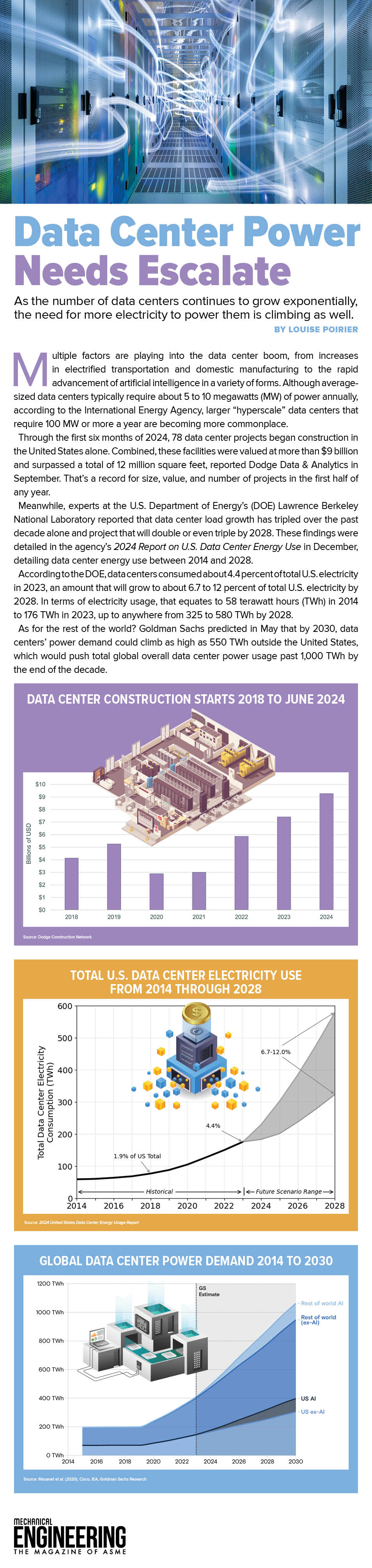

This infographic, titled 'Data Center Power Needs Escalate' (Jan 21, 2025), visualizes U.S. and global data-center electricity use and forecasts (2014–2028/2030), highlighting how rapidly rising power demand creates a bottleneck for deploying large GPU clusters and hyperscale AI capacity — directly illustrating the tweet’s point that power and infrastructure limit AI compute scale. ([asme.org](https://www.asme.org/getmedia/02a1e495-6db6-4069-848f-b128f357f5e0/0121_infographic-shifting-sources-for-electric-generation.jpg?ext=.jpg&height=4020&width=954))

Source: ASME (American Society of Mechanical Engineers)

Research Brief

What our analysis found

Google Cloud's leadership has openly acknowledged that surging AI demand is outstripping the company's ability to deploy infrastructure. CEO Sundar Pichai confirmed in Q1 2026 that the cloud division is "compute constrained in the near-term" and that revenue "would have been higher with more capacity." Despite these constraints, Google Cloud still posted 63% year-over-year revenue growth to over $20 billion in the quarter, with its cloud backlog nearly doubling to more than $460 billion — a staggering gap between contracted demand and deliverable supply. Google Cloud VP Amin Vahdat has said the company must double its AI serving capacity every six months and deliver 1,000 times more compute, storage, and networking capacity within five years just to keep pace.

This structural shortfall is fueling a gold rush among a new class of AI infrastructure companies. CoreWeave now carries a contracted revenue backlog of $66.8 billion, Nebius has assembled over $46 billion in commitments anchored by Microsoft and Meta, and TeraWulf has locked in approximately $6.7 billion in Fluidstack leases backed by a $3.2 billion Google credit enhancement. Meanwhile, former Bitcoin miners like Iris Energy and Cipher Mining are repurposing cheap power assets into GPU cloud capacity, with Iris Energy projecting over $3.7 billion in annualized AI cloud revenue by year-end 2026 and Cipher signing a separate $5.5 billion, 15-year lease with AWS.

The pattern extends beyond raw infrastructure. DigitalOcean launched its AI-Native Cloud in April 2026 targeting the inference and agentic computing layer, reporting AI customer ARR up 150% year-over-year to $120 million and inference services ARR surging 254% year-over-year. Applied Digital's Polaris Forge 1 campus in North Dakota has its full 400 MW of critical IT load contracted to CoreWeave under leases worth an estimated $11 billion. The bottleneck Google described is clearly not theoretical — it is reshaping capital flows across the entire AI compute supply chain.

Fact Check

Evidence from both sides

Supporting Evidence

Google explicitly confirmed the capacity bottleneck

Sundar Pichai stated in Q1 2026 earnings that Google Cloud is "compute constrained in the near-term" and that revenue would have been higher with more capacity, directly corroborating the tweet's central premise.

Google Cloud backlog nearly doubled to over $460 billion

The massive gap between contracted demand and deployed infrastructure validates the claim that demand is far outpacing supply, creating opportunity for third-party builders.

NVIDIA's $2 billion investment in Nebius is confirmed

NVIDIA made a $2 billion investment in Nebius in March 2026, and Nebius holds a combined potential backlog exceeding $46 billion through its Microsoft ($17.4B–$19.4B) and Meta ($27B) partnerships.

Iris Energy's Microsoft deal and GPU buildout are substantiated

Iren secured a $9.7 billion cloud capacity deal with Microsoft in November 2025, has ordered over 50,000 NVIDIA B300 GPUs targeting approximately 150,000 total chips, and projects over $3.7 billion in annualized AI cloud revenue by year-end 2026 — slightly exceeding the tweet's $3.4 billion figure.

CoreWeave's $66.8 billion contracted backlog is verified

CoreWeave reported this figure as of March 2026, with expanded commitments from Meta ($21B), Anthropic, and OpenAI, closely aligning with the tweet's ~$67 billion claim.

Cipher Mining's Google-backed Fluidstack deals and AWS contract are confirmed

Google backstops Fluidstack obligations and holds an approximately 5.4% equity stake in Cipher, while AWS signed a separate $5.5 billion, 15-year lease for 300 MW — matching the tweet's claims.

TeraWulf's Lake Mariner and Abernathy contracts are substantiated

TeraWulf secured approximately $6.7 billion in Fluidstack leases backed by a $3.2 billion Google credit enhancement at Lake Mariner, and the Abernathy JV adds 168 MW over 25 years representing roughly $9.5 billion in contracted revenue with $1.3 billion of Google lease support.

DigitalOcean's AI metrics match the tweet's claims

AI customer ARR was confirmed up 150% year-over-year to $120 million in Q4 2025, and the company launched its AI-Native Cloud targeting inference and agentic workloads in April 2026.

The bottleneck is industry-wide, not just Google

Microsoft Azure and Amazon Web Services have reported similar capacity constraints, reinforcing the thesis that demand overflow benefits independent infrastructure builders.

Contradicting Evidence

Some revenue figures are projections, not confirmed revenue

Numbers like Iris Energy's $3.4–$3.7 billion ARR by year-end 2026 and Applied Digital's $11 billion in expected revenue from CoreWeave are forward-looking estimates, not realized revenue. Contracted backlogs can be renegotiated, delayed, or cancelled, meaning actual revenue may differ significantly from stated commitments.

Google's constraint may be temporary, not structural

Google Cloud's Thomas Kurian suggested demand could exceed supply for years, but Google is simultaneously investing heavily in its own infrastructure buildout. As hyperscalers scale their own capacity, the overflow benefiting third-party providers could diminish, potentially stranding some of the infrastructure these companies are racing to build.

The tweet's framing of Lake Mariner as $3.2B in Google guarantees slightly oversimplifies the structure

The $3.2 billion figure is a credit enhancement backing Fluidstack's lease obligations, not a direct Google contract with TeraWulf. The counterparty risk ultimately flows through Fluidstack, adding a layer of intermediary complexity the tweet does not acknowledge.

Cipher Mining's Barber Lake capacity claim of 300 MW conflates multiple deals

Research confirms a 168 MW Fluidstack colocation agreement expandable to $7 billion plus an additional 39 MW Fluidstack deal, while the separate 300 MW allocation is the AWS contract — the tweet's description of "300 MW fully contracted with Fluidstack" at Barber Lake may overstate the single-site Fluidstack commitment.

DigitalOcean operates at a dramatically different scale than the other companies listed

With $120 million in AI customer ARR, DigitalOcean's AI revenue is orders of magnitude smaller than the multi-billion-dollar backlog figures cited for CoreWeave, Nebius, and others, making its inclusion alongside these names potentially misleading about relative market impact.

Bitcoin-to-AI pivot companies face significant execution risk

Companies like Iris Energy, Cipher Mining, and TeraWulf are transitioning from cryptocurrency mining to AI data centers, a fundamentally different operational challenge involving GPU deployment, cooling infrastructure, and enterprise-grade SLAs — execution against contracted backlogs is far from guaranteed.

Concentration risk is substantial across these companies

Many of the cited firms depend heavily on a small number of customers — CoreWeave on OpenAI and Meta, Iris Energy and TeraWulf on Microsoft and Google-backed Fluidstack, Applied Digital on CoreWeave — meaning the loss or renegotiation of a single contract could materially impair projected revenue.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.