AI infrastructure stocks are booming: AI infrastructure stocks have outperformed the equal-weight S&P 500 by +115% since December 2023, more than any other AI-related category. This group covers semiconductors, data center operators, cloud providers, networking equipment firms, and power companies, among others. This is followed by a +45% outperformance from mega-cap hyperscalers, including Microsoft $MSFT, Alphabet $GOOGL, Amazon $AMZN, and Meta $META. AI productivity stocks, which track companies using AI to cut costs and boost efficiency rather than build the technology, have outperformed by +10% over the same period. Meanwhile, software names have been the weakest group, trailing the average stock by -20%. AI infrastructure stocks are driving the revolution.

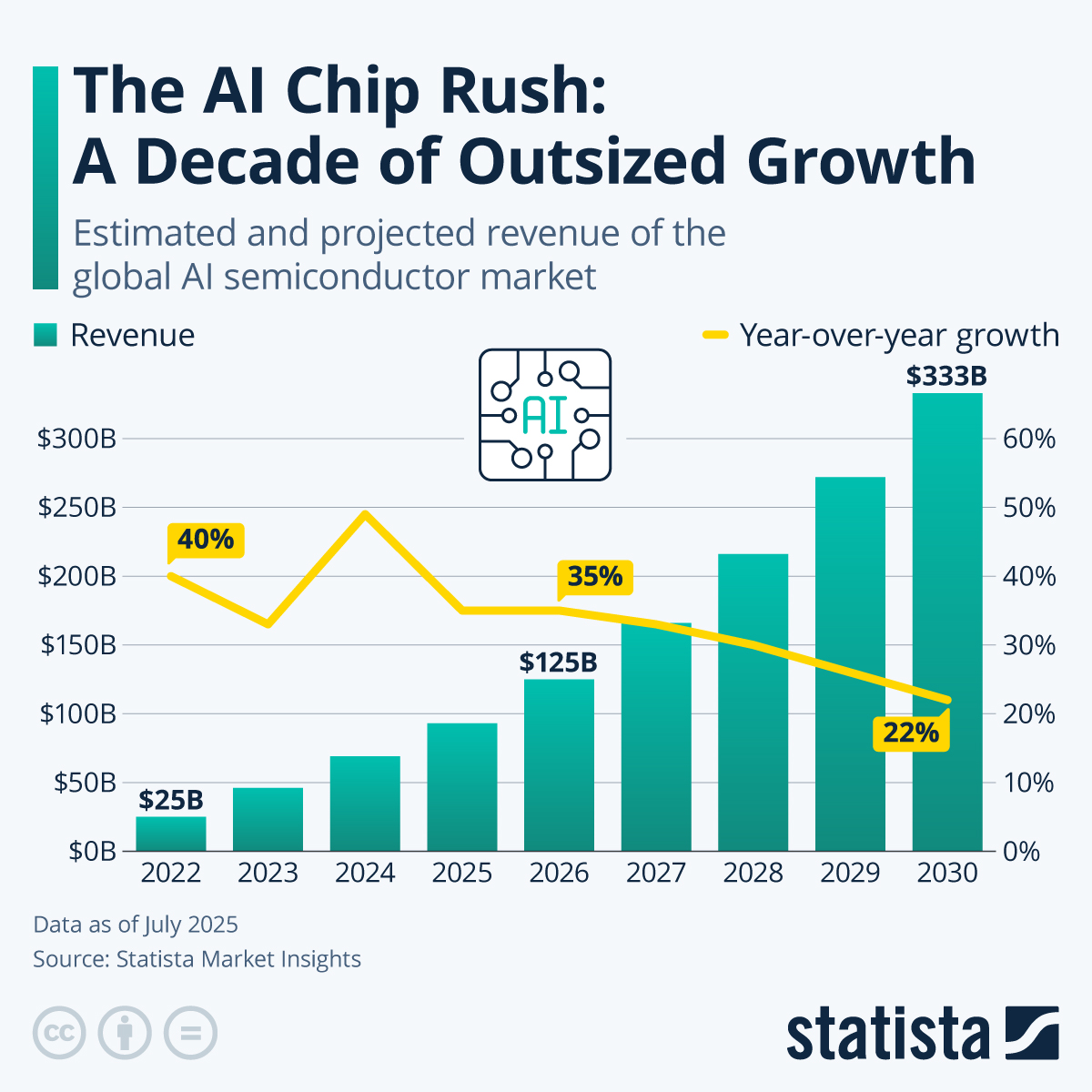

This infographic (bar + line chart) shows estimated and projected revenue for the global AI semiconductor market (2022–2030), highlighting rapid growth (e.g., $25B in 2022 to $333B by 2030). It directly supports the ‘AI infrastructure’ claim by visualizing the outsized demand and revenue tailwind for semiconductors — a core component of the AI infrastructure stock group (chips that power data centers, clouds and networking equipment).

Source: Statista

Research Brief

What our analysis found

AI infrastructure stocks have emerged as the dominant force in equity markets, dramatically outpacing the broader index since late 2023. The underlying market fundamentals support this surge: the AI infrastructure market is projected to balloon from $135.81 billion in 2024 to as much as $394.46 billion by 2030, representing a compound annual growth rate of 19.4%. Spending on compute and storage hardware for AI deployments alone jumped 97% year-over-year in the first half of 2024, reaching $47.4 billion, with servers equipped with AI accelerators experiencing a staggering 178% growth during the same period. As of April 2026, AI-linked stocks in the data center, semiconductor, and energy sectors now comprise over 40% of the S&P 500's total value.

The hyperscaler spending boom is a key catalyst. Microsoft, Amazon, Alphabet, and Meta have collectively committed over $440 billion to AI capabilities within a 12-month window, with Goldman Sachs projecting that AI infrastructure investments will contribute roughly 40% of all S&P 500 earnings growth in 2026. Semiconductors have been a standout performer, with the VanEck Semiconductor ETF surging 27.73% year-to-date in 2026 compared to the S&P 500's 4.07%. Utilities stocks, buoyed by massive data center power demands, have risen 44% since late 2023, making them the third-best performing S&P 500 sector.

However, the rally is not without risks. The extreme concentration of market value in a handful of AI-driven companies creates systemic vulnerability, and some software names have struggled as investors rotate capital toward infrastructure plays. Reports in early 2026 described a so-called "SaaS-Pocalypse" as capital flowed out of AI-sensitive software stocks into companies building the physical backbone of the AI revolution. Meanwhile, a notable 74% of companies report dissatisfaction with their current GPU utilization, raising questions about whether infrastructure spending is running ahead of actual deployment efficiency.

Fact Check

Evidence from both sides

Supporting Evidence

Broad AI stock outperformance since ChatGPT's launch

AI-related firms have collectively gained 200% since ChatGPT debuted in late 2022, dramatically outperforming the remaining S&P 500 companies, which averaged only a 27% gain over the same period. The S&P 500 would reportedly be trading about 25% lower without the AI boost.

Semiconductor sector dominance

The semiconductor industry recorded a 28.8% gain over six months leading to April 2026, while the S&P 500 declined by 2.3%. Individual performers include AMD up 40.42% YTD, Micron up 68.23% YTD, and Intel up 79.68% YTD in 2026. Nvidia became the first $5 trillion company in 2025.

Utilities and power producers surging on data center demand

Utilities stocks have collectively risen 44% since late 2023, becoming the third-best performing S&P 500 sector. Independent power producers NRG Energy rose 85% in 2025, Constellation Energy gained 65%, and Vistra Corp. jumped 41%.

Hyperscaler capital commitments validate infrastructure thesis

Microsoft, Amazon, Alphabet, and Meta committed over $440 billion to AI capabilities within 12 months as of January 2026, with collective AI investment projected to reach nearly $700 billion in 2026. Alphabet shares rose 184% over five years, outperforming the S&P 500's 65% return.

AI productivity stock outperformance aligns with tweet's claim

Publicly traded companies adopting productivity AI outperformed the S&P 500 by 29% from July 2024 to July 2025, with stock prices increasing 17.2% versus the S&P 500's 13.3%, consistent with the tweet's reported +10% outperformance category.

Massive hardware spending growth

Spending on compute and storage hardware for AI deployments increased 97% year-over-year in the first half of 2024, reaching $47.4 billion, with AI accelerator servers growing 178% and expected to exceed 75% of server AI infrastructure spending by 2028.

Contradicting Evidence

Exact +115% outperformance figure is not independently verified

While the general magnitude of AI infrastructure outperformance is well-documented across multiple data points, the precise claim of +115% outperformance versus the equal-weight S&P 500 since December 2023 is not directly corroborated with that specific figure and benchmark in available market data.

Software underperformance of -20% lacks precise sourcing

The claim that software names trailed the average stock by -20% is not explicitly confirmed with that exact percentage. However, reports from early 2026 describing a "SaaS-Pocalypse" and investor rotation out of AI-sensitive tech into AI-immune sectors lend indirect support to software weakness.

Dangerous market concentration poses systemic risk

AI stocks now comprise over 40% of the S&P 500's total market capitalization as of April 2026. This extreme concentration in a handful of companies means a downturn in major AI players could trigger widespread market deleveraging, suggesting the boom carries significant fragility.

Individual company struggles within booming sectors

Despite broad sector growth, specific semiconductor companies like Semtech Corp. and Kulicke and Soffa Industries have experienced declining operating margins, falling free cash flow, and decreased sales, demonstrating that rising tides have not lifted all boats equally.

GPU underutilization raises efficiency concerns

A significant 74% of companies report dissatisfaction with their current GPU and compute infrastructure utilization, suggesting that the massive capital spending on AI infrastructure may be outpacing organizations' ability to effectively deploy and use the technology they are purchasing.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.