I’m surprised markets aren’t pricing in long term disruption of card networks + interchange like $V and $MA. By $CRCL and $COIN. From Global Markets Head at Circle: "Over the past nine months, AI agents completed 140 million payments with a total transaction volume of 43 million US dollars. Among these, 98.6% were settled in USDC, with an average transaction amount of only 0.31 US dollars." Card networks and % fee payment processors like $PYPL are likely going to be cooked?

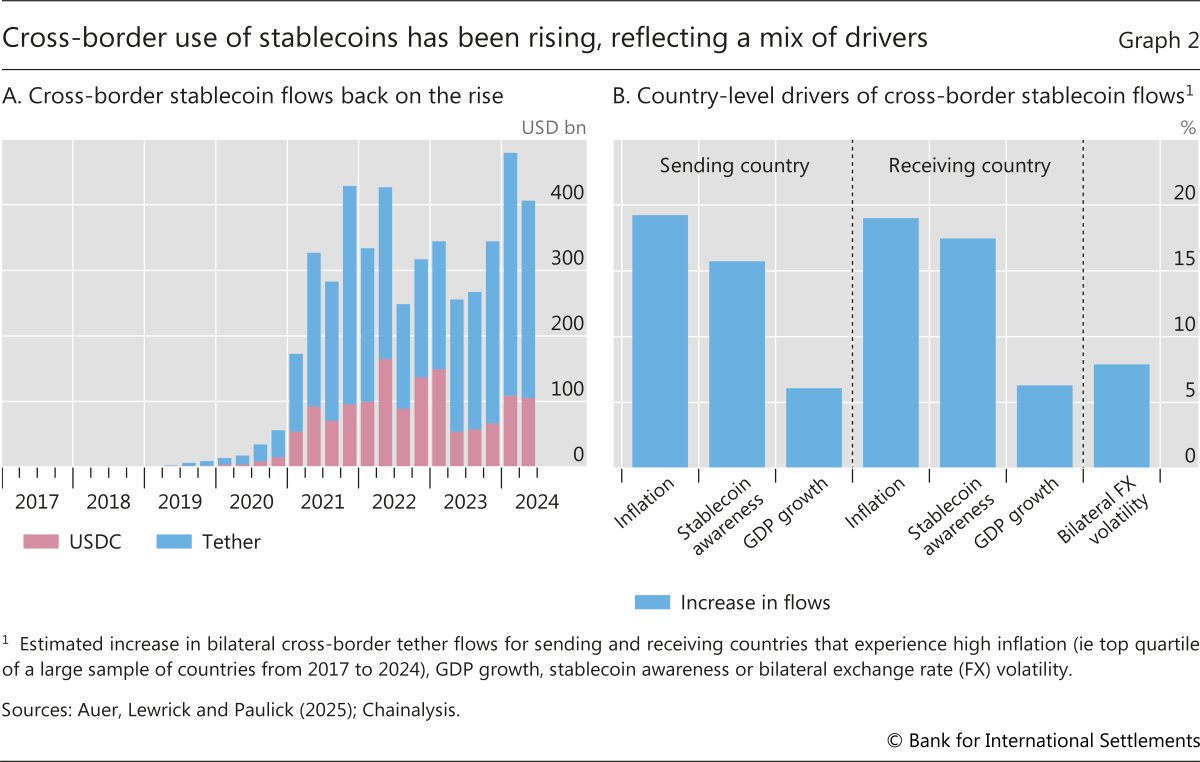

This BIS infographic (Annual Economic Report 2025, Graph 2) shows cross-border stablecoin use rebounding and rising sharply from 2017–2024, with USDC and Tether driving flows and macro factors like inflation and FX volatility as key drivers. It directly illustrates the growing use of stablecoins as payment rails—evidence that alternatives like USDC (Circle/Coinbase ecosystem) could erode traditional card-network and interchange models over time.

Source: Bank for International Settlements (BIS)

Research Brief

What our analysis found

A striking datapoint from Circle's Head of Global Markets, Peter Schroeder, has ignited debate over the future of card networks: over the past nine months, AI agents completed 140 million payments totaling $43 million, with 98.6% settled in USDC and an average transaction size of just $0.31. The figures, circulated widely in early March 2026, highlight a nascent but rapidly growing category of autonomous micropayments flowing entirely outside traditional card rails — transactions so small that conventional processing fees (e.g., Stripe's 2.9% + $0.30 per transaction) would consume nearly all or more than the payment's value.

The infrastructure enabling this shift is expanding quickly. Coinbase launched Agentic Wallets in February 2026 alongside its x402 protocol, an HTTP-based standard for per-request stablecoin payments. Alchemy built a system letting AI agents auto-pay for blockchain data and compute in USDC on Base. Meanwhile, Circle itself unveiled a "Nanopayments" testnet on March 10, 2026, supporting gas-free USDC transfers as small as $0.000001 — explicitly designed as a primitive for agentic commerce. Shopify's mid-2025 integration of USDC checkout via Stripe and Coinbase has further pushed stablecoin acceptance into mainstream merchant infrastructure.

Yet the scale remains embryonic relative to incumbents. The $43 million in agent payments is a rounding error next to global card network volumes, and Yahoo Finance noted in March 2026 that stablecoin firms are "betting big on AI agent payments that barely exist." Crucially, Visa and Mastercard are not standing still: Visa announced U.S. stablecoin settlement in December 2025 with a $3.5 billion annualized run rate, and Mastercard rolled out end-to-end stablecoin capabilities including USDC settlement across multiple regions. The question is whether incumbents can absorb the disruption or whether purpose-built crypto rails will capture the high-frequency, low-value payment layer that card economics structurally cannot serve.

Fact Check

Evidence from both sides

Supporting Evidence

Card fee economics break at micropayment scale

With an average AI-agent transaction of $0.31, traditional card processing fees like Stripe's 2.9% + $0.30 would consume nearly 100% of each payment. PayPal's micropayments rate of 5% + $0.05 still eats roughly 21% of a $0.31 transaction, making stablecoin rails dramatically more cost-effective for this use case.

Rapid infrastructure buildout for agent payments

Coinbase's Agentic Wallets and x402 protocol, Alchemy's USDC auto-pay system for blockchain services, and Circle's Nanopayments testnet (supporting transfers down to $0.

collectively lower integration friction for autonomous, per-request payment mode...

collectively lower integration friction for autonomous, per-request payment models that card networks were never designed to handle (cointelegraph.com, coinbase.com, circle.com).

Mainstream merchant adoption of stablecoin rails

Shopify's June 2025 partnership with Stripe and Coinbase to enable USDC payments — including a promotional 1% USDC cashback for U.S. customers — creates real optionality for merchants to route low-value transactions away from card networks (shopify.com).

Market already pricing in some risk

On February 24, 2026, Visa shares fell approximately 4.4–4.5% and Mastercard dropped 5.7–6.3% following a research note arguing AI-agent payments could bypass card fee structures, suggesting institutional investors are beginning to take the threat seriously (computing.net).

Incumbents' own moves validate the threat

Visa's December 2025 U.S. stablecoin settlement announcement and Mastercard's end-to-end stablecoin capabilities rollout implicitly acknowledge that programmable stablecoin rails offer cost and speed advantages that could erode interchange-based revenue if left unaddressed (usa.visa.com, mastercard.com).

Regulatory tailwinds

The GENIUS Act, signed into law on July 18, 2025, created a federal framework for payment stablecoins, reducing legal uncertainty and potentially accelerating enterprise and consumer adoption of USDC-based payment flows through 2026–27 (congress.gov).

Contradicting Evidence

Current scale is negligible

The $43 million in total AI-agent payments over nine months is immaterial compared to global card network volumes — Visa alone processes trillions of dollars annually. Yahoo Finance noted in March 2026 that stablecoin firms are "betting big on AI agent payments that barely exist" (finance.yahoo.com).

Incumbents are actively integrating stablecoins, not ignoring them

Visa expanded USDC settlement in the U.S. with a $3.5 billion annualized run rate as of November 2025, and Mastercard unveiled comprehensive stablecoin capabilities from wallets to checkout. These incumbents could absorb stablecoin innovation into their existing networks rather than be disrupted by it (usa.visa.com, mastercard.com).

Agent payments are overwhelmingly machine-to-machine, not consumer-facing

The 140 million transactions at $0.31 average are primarily API calls and compute micro-charges between AI systems — a category that never used card rails to begin with. This represents a new market segment rather than direct substitution of existing Visa and Mastercard transaction volume.

Card networks dominate consumer trust, compliance, and dispute resolution

Visa and Mastercard provide chargeback protections, fraud detection, regulatory compliance across jurisdictions, and consumer trust built over decades. Stablecoin rails currently lack equivalent consumer protection frameworks, limiting their ability to replace card networks for mainstream retail transactions.

Circle's revenue model depends on interest income, not payments disruption

Circle's FY2025 revenue of $2.7 billion is overwhelmingly driven by reserve income from Treasury holdings backing USDC, not from payment processing fees. The company's financial incentives are aligned with USDC circulation growth, which may not directly translate into card-network displacement (circle.com).

Network effects and merchant acceptance create enormous switching costs

Card networks benefit from entrenched two-sided network effects with billions of cards in circulation and millions of merchant acceptance points globally. Even with lower per-transaction costs, stablecoin payment rails face a massive adoption gap before they could meaningfully redirect transaction volume away from incumbents.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.