𝗧𝗵𝗲 𝗯𝗶𝗴𝗴𝗲𝘀𝘁 𝗔𝗜 𝗿𝗶𝘀𝗸 𝗶𝗻 𝘁𝗲𝗰𝗵 𝗺𝗮𝘆 𝘀𝗶𝘁 𝗼𝗻 𝘀𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗯𝗮𝗹𝗮𝗻𝗰𝗲 𝘀𝗵𝗲𝗲𝘁𝘀. A massive debt wall is forming across the software sector. Between 𝟮𝟬𝟮𝟲 𝗮𝗻𝗱 𝟮𝟬𝟮𝟵, 𝗻𝗲𝗮𝗿𝗹𝘆 $𝟭𝟬𝟬𝗕 𝗶𝗻 𝘀𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗹𝗼𝗮𝗻𝘀 𝗺𝗮𝘁𝘂𝗿𝗲. 🥶 The largest concentration arrives in 𝟮𝟬𝟮𝟴 𝘄𝗶𝘁𝗵 𝗿𝗼𝘂𝗴𝗵𝗹𝘆 $𝟰𝟬𝗕 𝗰𝗼𝗺𝗶𝗻𝗴 𝗱𝘂𝗲. The credit quality tells the real story. A large share of this debt sits deep in 𝗕, 𝗕-, 𝗮𝗻𝗱 𝗖𝗖𝗖 𝘁𝗲𝗿𝗿𝗶𝘁𝗼𝗿𝘆, 𝘄𝗶𝘁𝗵 𝗮𝗿𝗼𝘂𝗻𝗱 𝗵𝗮𝗹𝗳 𝗿𝗮𝘁𝗲𝗱 𝗕- 𝗼𝗿 𝗹𝗼𝘄𝗲𝗿. This structure made sense during the zero-interest era. Private credit funds financed software companies because the model looked structurally safe. Recurring subscriptions created predictable cash flows, and rising valuations supported aggressive lending. AI changes that equation. AI platforms compress entire software stacks. Tasks that once required multiple SaaS products increasingly run through a single AI layer. That shift creates a structural change. The number of software tools companies need may decline. For highly leveraged vendors, this creates a refinancing challenge. Debt raised during the growth cycle eventually demands real cash flow. This is where systemic risk appears. Software represents about 𝟭𝟮% 𝗼𝗳 𝘁𝗵𝗲 𝗹𝗲𝘃𝗲𝗿𝗮𝗴𝗲𝗱 𝗹𝗼𝗮𝗻 𝗺𝗮𝗿𝗸𝗲𝘁, making it the largest single sector exposure. If AI accelerates consolidation across SaaS, the ripple effects extend far beyond Silicon Valley. India sits at the center of that ecosystem. India’s $𝟯𝟬𝟬𝗕+ 𝘁𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝘆 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝘆, 𝗵𝗲𝗮𝗱𝗶𝗻𝗴 𝘁𝗼𝘄𝗮𝗿𝗱 $𝟯𝟱𝟬𝗕, operates a large share of the world’s enterprise software infrastructure. Any restructuring or consolidation across SaaS influences implementation spending, vendor ecosystems, and enterprise technology budgets. AI will create enormous productivity gains. Before that equilibrium forms, the software industry may pass through something else first. 𝗔 𝗯𝗮𝗹𝗮𝗻𝗰𝗲 𝘀𝗵𝗲𝗲𝘁 𝗿𝗲𝘀𝗲𝘁 👀 The intersection of 𝗔𝗜 𝗱𝗶𝘀𝗿𝘂𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗹𝗲𝘃𝗲𝗿𝗮𝗴𝗲𝗱 𝗰𝗮𝗽𝗶𝘁𝗮𝗹 𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲𝘀 could define the next phase of the global software market. 𝟮𝟬𝟮𝟴 𝗺𝗮𝘆 𝗯𝗲𝗰𝗼𝗺𝗲 𝘁𝗵𝗲 𝘆𝗲𝗮𝗿 𝘁𝗵𝗼𝘀𝗲 𝘁𝘄𝗼 𝗳𝗼𝗿𝗰𝗲𝘀 𝗰𝗼𝗹𝗹𝗶𝗱𝗲.

Source: Federal Reserve Board (FEDS Notes)

Research Brief

What our analysis found

The tweet's central thesis — that a massive wall of low-rated software debt is maturing into an era of AI-driven disruption — is well-supported by major Wall Street research. Morgan Stanley estimates software accounts for roughly 16% of the $1.5 trillion U.S. leveraged loan market (~$235 billion), making it the single largest sector exposure. Critically, about half of that debt is rated B- or lower, according to both Morgan Stanley and JPMorgan analyses. JPMorgan has specifically flagged ~$51 billion in B- or lower software loans maturing in 2028 and another ~$50 billion in 2029, meaning the tweet's "nearly $100 billion" figure may actually be conservative when accounting for all rating tiers across the 2026–2029 window.

The AI disruption angle is where the picture gets more nuanced. A sharp early-2026 selloff in software loans — Voya reported the software segment returned -2.97% in January 2026 alone — shows the market is already pricing in AI displacement risk. CLO managers are actively scrubbing portfolios for vulnerable software credits, and Blue Owl raised its withdrawal cap to 17% at a tech-focused fund amid elevated redemption requests. However, Gartner still forecasts worldwide software spending to rise ~14.7% in 2026 to approximately $1.43 trillion, and enterprise SaaS portfolio data from Zylo shows app counts holding roughly flat at ~305. The refinancing risk for low-rated software borrowers is real and documented; the scale and speed of AI-driven revenue erosion across the broader SaaS sector remains an open and hotly debated question.

The India connection is directionally accurate. NASSCOM pegs India's tech industry revenues at approximately $315 billion for FY26, with significant enterprise software implementation and support operations. Any restructuring wave across SaaS vendors would ripple into India's implementation spending, vendor partnerships, and enterprise technology budgets — though India's diversification into AI services and Global Capability Centers may partially offset that exposure.

Fact Check

Evidence from both sides

Supporting Evidence

Software is the largest single sector in the U.S. leveraged loan market.

PitchBook/LCD data from July 2025 shows a 12.3% share; Morgan Stanley's February 2026 estimate puts it higher at ~16% of the ~$1.5 trillion market (~$235 billion in software loans). Both confirm the tweet's "~12%" claim as accurate-to-conservative.

About half of software debt is rated B- or lower.

Morgan Stanley explicitly states that roughly 50% of software loans carry B- or lower ratings, corroborated by JPMorgan's granular maturity analysis. S&P Global further notes software is the largest sector in both BSL CLOs (14.7%) and middle-market CLOs (19.2%).

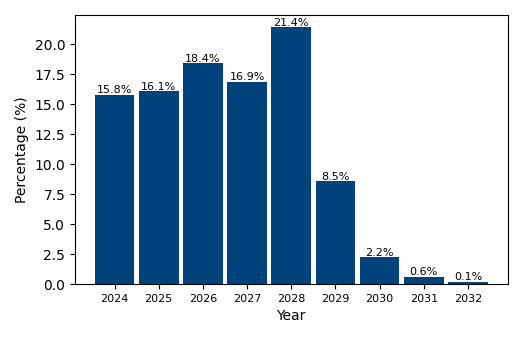

The 2028 maturity concentration is confirmed by multiple sources.

LPL Research shows ~25% of software debt matures in 2028, while JPMorgan flags ~$51 billion of B- or lower software loans coming due that year and another ~$50 billion in 2029. Morgan Stanley notes ~30% of software loans mature by 2028, versus ~22% for the broader market — a meaningfully front-loaded schedule.

The market has already begun repricing software credit risk.

Voya reported software loans returned -2.97% in January 2026 with average bids falling 364 basis points. TwentyFour Asset Management documented meaningful CLO repricing as investors reassessed software exposure and the 2028 maturity wall.

Real-world liquidity stress has emerged.

Blue Owl raised its withdrawal cap to 17% at its tech-focused fund amid redemption requests reaching ~15% of NAV, and subsequently sold ~$1.4 billion of loans across its BDCs at ~99.7% of par to meet payouts — a concrete sign of investor anxiety around software credit.

JPMorgan has explicitly warned about AI risk inside CLO structures.

Strategy notes flagged up to ~$150 billion of loans in CLOs as potentially exposed to AI-related disruption risk, with software as the primary sector of concern.

India's tech industry scale is confirmed.

NASSCOM's latest figures peg India's technology industry at ~$315 billion in FY26, heading toward $350 billion, with substantial enterprise software implementation and support operations that would be affected by SaaS vendor consolidation.

Contradicting Evidence

Global software spending is still growing robustly.

Gartner forecasts worldwide software spending to rise ~14.7% in 2026 to approximately $1.43 trillion, suggesting broad-based demand destruction is not yet materializing and many software companies — including those embedding AI features — continue to grow revenue.

Enterprise app counts have not collapsed.

Zylo's 2024 SaaS Management Index shows enterprise software portfolios averaging ~305 applications with essentially flat counts heading into 2026, indicating that "stack compression" from AI remains more theoretical than observed at scale so far.

Private credit managers argue losses are contained.

Blue Owl's leadership publicly stated that current market loss assumptions are "disconnected from portfolio math," pointing to low loan-to-value ratios (~30%) and equity value gains since origination as cushions against credit losses.

Default rates are not projected to spike.

Fitch projected U.S. leveraged loan defaults to ease slightly by end-2026 to 4.5–5.0%, suggesting a challenging but manageable environment rather than a systemic collapse scenario. BlackRock data shows only ~32% of all USD loans (across sectors) are rated B- or below.

CLO exposure to software is lower than the headline index weight.

TwentyFour Asset Management notes average software exposure in U.S. CLOs is ~10% — below the 12–16% index weight — while Barrow Hanley confirms BSL CLOs tend to underweight software relative to the broader loan index, mitigating systemic transmission risk.

AI may be a tailwind for select software companies, not a uniform threat.

Morgan Stanley specifically argued AI is a tailwind for companies like Atlassian even amid the broader sector selloff, indicating a winner-loser dynamic rather than blanket SaaS destruction.

Amend-and-extend activity has already reshaped the maturity wall.

PitchBook/LCD and other sources document record amend-and-extend activity in 2024–2025, which has pushed many near-term maturities into later years. While this concentrates risk in 2028, it also means companies have already bought additional runway — the wall is partly a product of proactive management, not neglect.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.