Q1 earnings are in: 2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business: Search queries are at an all-time high with AI continuing to drive usage. Google Cloud revenue grew 63%, Gemini models have incredible momentum, and it was our strongest quarter ever for consumer AI subs, driven by @GeminiApp. Thanks to our partners + employees around the world. Much more to share on our earnings call in 20 minutes… and at Google I/O in 20 days!

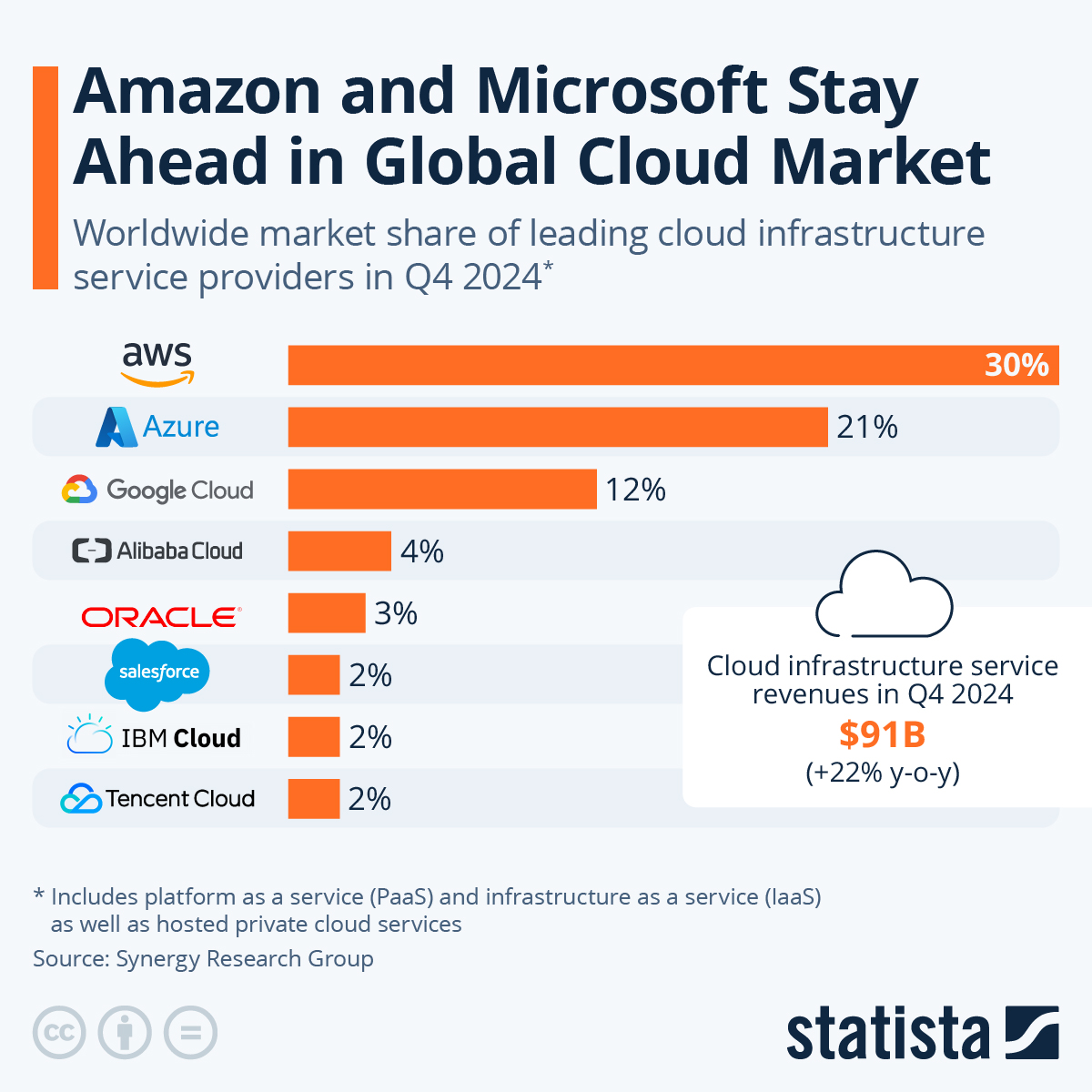

This Statista infographic shows worldwide market share of leading cloud infrastructure providers (Q4 2025), highlighting Google Cloud’s position among the hyperscalers and the accelerating cloud market. It provides visual context for the tweet’s claims about strong Google Cloud momentum and rising AI-driven cloud demand (which underpins the 63% YoY cloud revenue growth noted in the earnings update).

Source: Statista

Research Brief

What our analysis found

Alphabet Inc. posted a commanding Q1 2026 earnings report, with consolidated revenues reaching $109.9 billion, a 22% year-over-year increase. Operating income surged 30% to $39.7 billion, pushing the operating margin to 36.1%. Net income skyrocketed 81% to $62.6 billion, delivering diluted EPS of $5.11 — nearly double the analyst consensus of $2.63. CEO Sundar Pichai pointed to the company's AI-first strategy as the catalyst behind gains across virtually every business segment.

Google Cloud was a standout performer, generating $20 billion in revenue with 63% year-over-year growth, while its backlog nearly doubled quarter-over-quarter to exceed $460 billion. Revenue from products built on Google's generative AI models grew nearly 800% year-over-year, and the company's first-party AI models now process over 16 billion tokens per minute via direct API use. Google Search advertising revenue also climbed 19% to $60.4 billion, with Pichai crediting AI-powered features like AI Mode and AI Overviews for pushing search queries to all-time highs.

However, the triumphant tone of Pichai's tweet belies some investor unease. Alphabet's stock slipped 0.61% in after-hours trading as Wall Street digested a raised full-year capital expenditure guidance of $180 billion to $190 billion, up from a prior range of $175 billion to $185 billion. The net income figure was also significantly inflated by a $36.9 billion unrealized gain on non-marketable equity securities, a one-time item that made the bottom-line growth appear more dramatic than the underlying operational improvement. Meanwhile, Google's Network advertising revenues declined 4%, and the Other Bets segment continued to lose money, posting a $2.1 billion operating loss.

Fact Check

Evidence from both sides

Supporting Evidence

Google Cloud's 63% revenue growth is verified

Multiple financial reports confirm Google Cloud reached $20 billion in Q1 2026 revenue, representing 63% year-over-year growth driven by surging demand for AI infrastructure and services.

Search queries hit all-time highs

CEO Sundar Pichai stated during the earnings call that AI-driven features such as AI Mode and AI Overviews are fueling increased Search usage, corroborating the claim that queries reached record levels.

Record quarter for consumer AI subscriptions

Pichai directly confirmed in the earnings release that Q1 2026 was Alphabet's strongest quarter ever for consumer AI plans, with the Gemini App cited as the primary driver. Total paid subscriptions across YouTube, Google One, and other services reached 350 million.

Gemini enterprise momentum is substantiated

Paid monthly active users for Gemini Enterprise grew 40% quarter-over-quarter, while Google's first-party AI models saw API token processing increase 60% from the prior quarter to over 16 billion tokens per minute.

Broad financial outperformance supports "terrific start"

Consolidated revenue of $109.9 billion beat expectations, operating income rose 30%, and diluted EPS of $5.11 nearly doubled the analyst consensus of $2.63, lending credibility to Pichai's characterization of a strong quarter.

Contradicting Evidence

Stock declined despite strong results

Alphabet shares fell 0.61% in after-hours trading following the earnings release, reflecting investor anxiety over the company's massive and rising AI capital expenditure commitments rather than pure enthusiasm for the results.

Net income inflated by a one-time gain

The headline 81% surge in net income was significantly boosted by a $36.9 billion net unrealized gain on non-marketable equity securities, meaning the operational improvement, while real, was far less dramatic than the bottom-line figure suggests.

Escalating capital expenditures raise profitability questions

Alphabet raised its full-year 2026 CapEx guidance to $180–$190 billion and signaled CapEx will "significantly increase" again in 2027, creating uncertainty about whether AI investments will generate commensurate returns.

Network advertising revenue declined

Google's Network advertising revenues fell 4% year-over-year, indicating that not literally "every part of the business" is benefiting from the AI push, as Pichai's tweet implies.

Other Bets remain deeply unprofitable

The Other Bets segment posted a $2.1 billion operating loss on just $411 million in revenue, a persistent drag that tempers the narrative of universal business strength.

Wiz acquisition expected to pressure Cloud margins

The recently completed acquisition of cloud security firm Wiz is projected to create a low single-digit percentage point headwind to Google Cloud's operating margin for the rest of 2026, potentially offsetting some of the segment's impressive growth trajectory.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.