$SNDK made more profit in one quarter than it made across the prior three years combined. Agentic AI is driving demand for NAND-backed storage across inference workloads, with SanDisk’s high-capacity enterprise SSDs positioned as a key part of the stack. https://t.co/ONSVs5VIYV

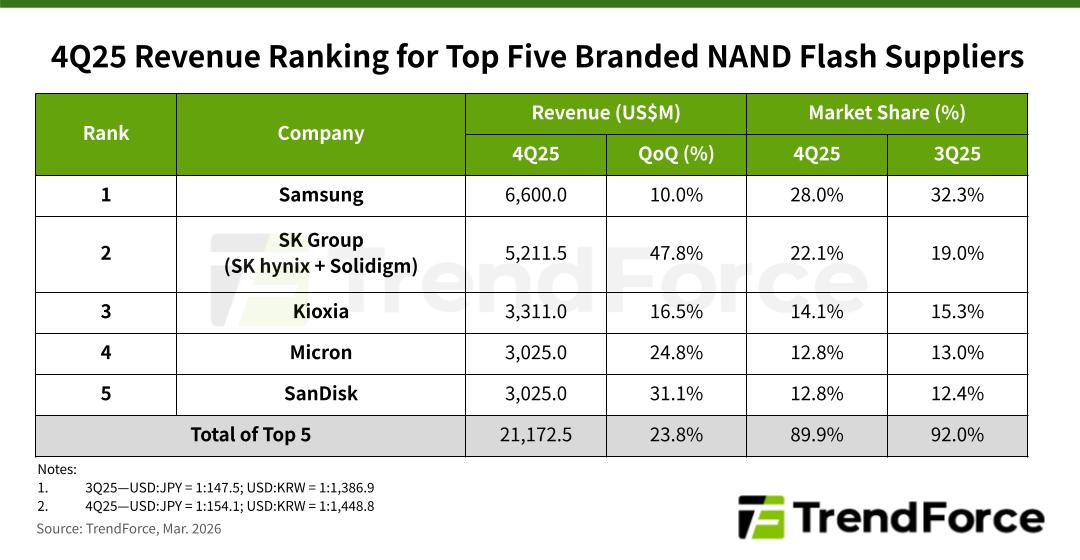

A TrendForce chart titled “4Q25 Revenue Ranking for Top Five Branded NAND Flash Suppliers” showing revenue (US$M), QoQ growth, and market share — it highlights SanDisk at ~$3.03B revenue and +31.1% QoQ. This directly illustrates the recent, AI-driven surge in NAND/enterprise-SSD revenue (which underpins the tweet’s claim about SanDisk benefiting from AI/inference demand).

Source: TrendForce

Research Brief

What our analysis found

SanDisk's fiscal Q3 2026 earnings report, released on April 30, 2026, revealed a company transformed by the AI infrastructure boom. The newly independent firm posted $5.95 billion in revenue, a staggering 251% increase year-over-year, and reported GAAP net income of $3.62 billion — a dramatic reversal from a $1.93 billion net loss in the same quarter a year earlier. Non-GAAP diluted EPS reached $23.41, significantly exceeding analyst expectations and underscoring the scale of the turnaround.

The engine behind the surge is datacenter demand driven by AI workloads. SanDisk's datacenter revenue hit $1.47 billion in Q3 2026, representing a 645% year-over-year increase and a 233% sequential gain. CEO David Goeckeler called the quarter a "fundamental inflection point," as the company pivoted aggressively toward high-value enterprise SSDs for cloud and AI infrastructure. GAAP gross margins expanded to 78.4%, up from just 22.5% a year prior, fueled by rising NAND average selling prices and a structural shift away from commoditized consumer markets.

Looking ahead, SanDisk has issued bullish guidance for Q4 2026, forecasting revenue between $7.75 billion and $8.25 billion and non-GAAP EPS of $30.00 to $33.00. The company has also secured long-term partnerships worth at least $42 billion and plans to begin shipping its QLC Stargate solutions for datacenter customers. Despite these results, shares slipped 6% in after-hours trading, suggesting some investors had priced in even more aggressive growth.

Fact Check

Evidence from both sides

Supporting Evidence

Massive quarterly profit versus prior losses

SanDisk reported GAAP net income of $3.62 billion in Q3 2026, compared to a GAAP net loss of $1.93 billion in Q3 2025. Given the company was operating at a loss or marginal profitability for much of the prior three-year window, a single quarter of $3.62 billion in profit could plausibly exceed the cumulative total of preceding years.

Revenue more than tripled year-over-year

Q3 2026 revenue of $5.95 billion represented a 251% increase over the prior year and a 97% sequential gain, confirming an extraordinary acceleration in the business.

Datacenter revenue surged 645% year-over-year

AI infrastructure demand was the primary catalyst, with datacenter revenue reaching $1.47 billion in Q3 2026. CEO David Goeckeler explicitly attributed this to AI-driven demand and called it a "fundamental inflection point."

Enterprise SSD demand tied to Agentic AI workloads

The structural shift toward high-capacity, low-latency NAND flash for inference and agentic AI workloads has been widely documented as a key growth driver, supporting the tweet's claim about SanDisk's positioning in the AI storage stack.

NAND pricing recovery amplified margins

After years of commoditization and falling prices, NAND ASPs rose in the mid-30% range in Q2 2026, with manufacturing lines sold out through 2026, directly benefiting SanDisk's profitability and supporting the scale of the profit surge.

Contradicting Evidence

The "prior three years" claim is difficult to verify precisely

SanDisk only became an independent public company on February 21, 2025, meaning much of the "prior three years" falls within the period when its financials were consolidated inside Western Digital's reports. Standalone SanDisk profit data for the full three-year window is not readily available, making the exact comparison hard to confirm.

Broader NAND market recovery is a contributing factor

While AI demand is clearly a major driver, the entire NAND flash industry has been recovering from a severe downturn, with prices more than doubling in recent months. Attributing SanDisk's profit explosion solely to Agentic AI overstates AI's role and underplays cyclical market dynamics.

Stock dropped 6% despite the earnings beat

SanDisk shares fell in after-hours trading following the Q3 2026 report, indicating that some investors may have concerns about the sustainability of these margins or viewed the results as already priced in, tempering the narrative of uncomplicated success.

Prior-period losses inflate the comparison

Comparing a record profit quarter against years that included significant net losses — such as the $1.93 billion loss in Q3 2025 — makes the headline claim technically easier to achieve but potentially misleading about steady-state profitability trends.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.