Hoya Capital Perspective: Janus Living IPO & What It Signals for REITs Ahead of the upcoming Janus Living (NYSE: JAN) IPO, we wanted to share a few thoughts from our vantage point at @HoyaCapital on the transaction itself and what it signals more broadly for REIT fundamentals and capital markets. Bottom Line: After one of the most challenging multi-year periods for REITs in decades—defined by sharply higher interest rates, compressed valuations, and a near-complete shutdown in IPO activity—we view the Janus offering as a notable “green shoot” for the sector. Why this deal matters: A rare bright spot after a difficult cycle. * REITs have spent the past several years in a capital-constrained environment. The fact that this deal is coming to market at all is notable—and potentially signals early-stage normalization. * Potential reopening of the REIT IPO window. If well received, Janus could mark an inflection point for public REIT issuance—particularly for differentiated, asset-backed sectors with visible internal growth. * Private-pay real estate is leading the recovery. Senior housing fundamentals have improved meaningfully: occupancy gains, reaccelerating rent growth, and historically muted new supply. * Demographics are becoming a near-term driver. The Baby Boomer cohort is now entering prime senior housing years, turning a long-dated theme into a tangible earnings driver. On Janus specifically: A rare pure-play SHOP platform. Janus will consist of 34 communities (~10,400 units) carved out of Healthpeak, generating roughly $220M of annual NOI, the vast majority from entrance-fee “Life Plan” communities. What is a CCRC—and how is this different? Much of the portfolio is composed of Continuing Care Retirement Communities (CCRCs)—large, campus-style properties where residents pay a significant upfront entrance fee plus ongoing service fees in exchange for access to a continuum of care. That contrasts with the more common SHOP model (as seen in much of Welltower’s portfolio), which is typically lease-based with no large upfront fee and more direct exposure to rent growth and operating margins. That said, Janus’s portfolio is not a typical CCRC mix, given its heavy weighting toward independent living (typical of the SHOP model). Unlocking value that wasn’t being recognized. Senior housing had become a relatively small and harder-to-value segment within Healthpeak’s broader platform. This separation is a logical step to surface that value. Positioned as a growth platform. Janus is expected to launch with minimal leverage and has an identified ~$675M acquisition pipeline, primarily in rental senior housing. Valuation framework: Janus is targeting up to a $5B valuation, offering 37M shares at $18–$20 to raise roughly $740M. The IPO target (~$5B) implies a ~4.5% cap rate, which would: * Place Janus squarely in line with public REIT valuations, notably Welltower, which trades in the ~4.5%–5.0% implied cap rate range. This aligns with top-tier healthcare REIT multiples, where leading names trade at ~25x P/FFO (a sizable premium to the REIT sector average of around 16-18x) * The $5B valuation is likely at the upper end of the warranted valuation range in the near term, given that CCRC portfolios are not typically assigned the same premium valuation as the SHOP independent living portfolios. Relative to the simplistic “10% of DOC” implied valuation (~$2.2B), even a mid-range IPO outcome suggests substantial value creation through separation and multiple expansion. With minimal initial leverage, Janus would debut as a mid-to-large cap REIT with sufficient scale and float, particularly given DOC’s expected majority ownership but intention to leave meaningful public float. Bottom Line: In our view, Janus represents a convergence of several themes we’ve been highlighting: * Stellar senior housing fundamentals with structurally limited new supply * How some REITs are getting creative to unlock shareholder value amid persistent downward valuation pressures * Early signs that REIT capital markets may be thawing after a prolonged freeze It doesn’t mark the end of the challenges facing REITs, but it may be one of the first clear signals that the cycle is beginning to turn.

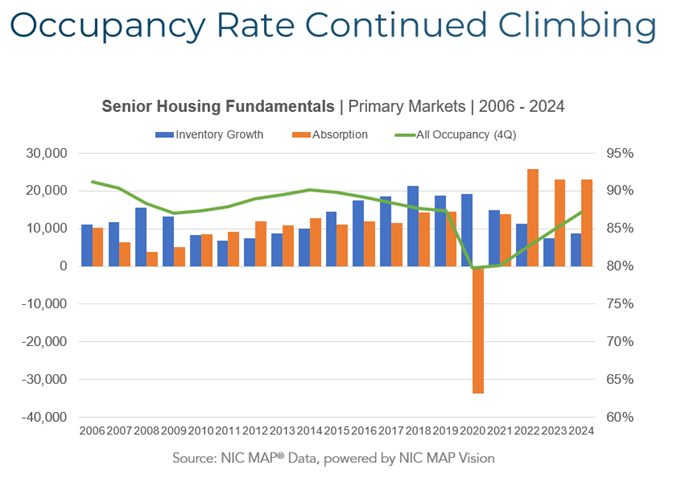

This NIC MAP Vision chart tracks U.S. senior housing fundamentals from 2006–2024, showing occupancy rebounding to 87.2% in 4Q 2024 alongside strong absorption and historically muted new supply. It directly supports the point that private‑pay senior housing fundamentals are improving ahead of the Janus Living IPO, signaling a more favorable backdrop for REITs in this segment.

Source: National Investment Center for Seniors Housing & Care (NIC)

Research Brief

What our analysis found

Healthpeak Properties (NYSE: DOC) announced the formation of Janus Living on January 7, 2026, following a confidential S-11 filing in December 2025. The company publicly filed its S-11 on February 27, 2026, with plans to list on the NYSE under the ticker "JAN." The initial portfolio comprises 34 senior housing communities with 10,422 units across 10 states, all operated under RIDEA structures. By unit mix, the portfolio skews heavily toward independent living at 43%, followed by assisted living at 20%, memory care at 9%, and skilled nursing at 9%. Roughly 69% of units are concentrated in Florida and Texas. BofA Securities and J.P. Morgan are serving as lead bookrunners.

The deal arrives amid improving senior housing fundamentals. According to NIC data, senior housing occupancy in the 31 Primary Markets reached 89.1% in Q4 2025, marking the 18th consecutive quarterly increase. Same-store asking rent growth ran at approximately 4.2–4.4% year-over-year in Q3 2025, while units under construction dropped to roughly 16,200 in 2025 from about 50,000 in 2019, underscoring historically constrained new supply. Demographically, the oldest Baby Boomers began turning 80 on January 1, 2026, entering the prime age cohort for independent and assisted living communities.

Healthpeak disclosed $220 million in annualized portfolio cash adjusted NOI as of Q3 2025 for the senior housing segment. Janus is expected to launch with leverage of less than 1x Net Debt/EBITDAre and has identified an approximately $675 million acquisition pipeline targeting stabilized cash NOI yields of 8–9%. The REIT IPO market has shown signs of revival: S&P Global counted 6 equity REIT debuts in 2024 and 3 in 2025, including major offerings like Lineage's $4.4–$5.1 billion IPO in July 2024 and American Healthcare REIT's $672 million IPO in February 2024. Healthpeak plans to retain majority ownership of Janus while leaving a meaningful public float, with current CEO Scott Brinker identified to lead the new entity.

Fact Check

Evidence from both sides

Supporting Evidence

REIT IPO market is recovering from a prolonged drought

S&P Global data confirms that equity REIT debuts rose from just 2 in 2022 and 3 in 2023 to 6 in 2024 and 3 in 2025, with major deals like Lineage's $4.4–$5.1 billion IPO and American Healthcare REIT's $672 million offering demonstrating renewed investor appetite for differentiated, asset-backed REITs.

Senior housing occupancy has improved meaningfully

NIC reports that Q4 2025 senior housing occupancy reached 89.1% in the 31 Primary Markets, the 18th straight quarterly increase, with Secondary Markets ending 2025 at 90.0%, confirming the tweet's claim of reaccelerating fundamentals.

New supply is historically muted

NIC data shows units under construction fell to approximately 16,200 in 2025 from about 50,000 in 2019, strongly supporting the tweet's assertion of structurally limited new supply.

Rent growth and operating margins are strengthening

NIC MAP cited same-store asking rent growth of approximately 4.2–4.4% year-over-year in Q3 2025, with operating margins exceeding 25% by mid-2025, validating the private-pay recovery narrative.

Baby Boomer demographics are becoming a near-term driver

Brookings research confirms that the oldest Baby Boomers started turning 80 on January 1, 2026, placing them squarely within typical entry ages for independent living and Life Plan communities.

Janus is structured as a pure-play SHOP platform

Healthpeak's filings confirm all 34 communities are operated under RIDEA structures with significant Life Plan (CCRC) exposure, and the portfolio's 43% independent living weighting validates the tweet's characterization of an atypical CCRC mix.

Minimal initial leverage and identified growth pipeline

Healthpeak filings confirm Janus will debut with less than 1x Net Debt/EBITDAre and has a roughly $675 million acquisition pipeline sourced in Q4 2025 targeting 8–9% stabilized Cash NOI yields.

$220 million annualized NOI figure is confirmed

Healthpeak's January 2026 investor presentation discloses $220 million in annualized portfolio cash adjusted NOI as of Q3 2025, matching the tweet's stated figure.

Contradicting Evidence

Specific IPO pricing terms and $5 billion valuation target are unconfirmed in public filings

The tweet cites a target of up to $5 billion in valuation with 37 million shares offered at $18–$20 to raise roughly $740 million, but Healthpeak's public S-11 filing did not disclose pricing terms, share counts, or a specific valuation target. These figures may reflect analyst estimates or pre-marketing guidance rather than confirmed offering details.

External management structure introduces costs and potential conflicts

The tweet does not mention that Janus will be externally managed by Healthpeak Investment Management, LLC, with a $10 million annual management fee. External management structures are generally viewed less favorably by REIT investors due to potential fee misalignment, which could weigh on the premium valuation the tweet implies.

The implied 4.5% cap rate comparison to Welltower may be imprecise

The tweet equates Janus's implied cap rate to Welltower's 4.5–5.0% range, but Welltower's portfolio is predominantly traditional SHOP with direct rent growth exposure, while Janus's heavy entrance-fee CCRC weighting generates revenue differently. As the tweet itself acknowledges, CCRC portfolios are not typically assigned the same premium as SHOP independent living portfolios, potentially making the top-end valuation optimistic.

Geographic concentration poses risk

Approximately 69% of Janus's units are concentrated in Florida and Texas, introducing meaningful exposure to regional economic, regulatory, and climate-related risks that could affect the growth narrative.

The NOI figure includes non-standard adjustments

Healthpeak's $220 million annualized figure includes non-refundable entrance fee cash collections in excess of GAAP amortization and the company's share of a joint venture. The GAAP-basis 2025 Adjusted NOI was $197 million, with $54 million in entrance fee cash exceeding amortization, suggesting the headline NOI figure may overstate recurring economic earnings.

Healthpeak's majority ownership limits true public market price discovery

With Healthpeak retaining majority ownership post-IPO, the free float may be constrained, potentially limiting the degree to which the IPO price reflects broad market demand rather than a controlled offering.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.