Hoya Capital Perspective: Janus Living IPO & What It Signals for REITs Ahead of the upcoming Janus Living (NYSE: JAN) IPO, we wanted to share a few thoughts from our vantage point at @HoyaCapital on the transaction itself and what it signals more broadly for REIT fundamentals and capital markets. Bottom Line: After one of the most challenging multi-year periods for REITs in decades—defined by sharply higher interest rates, compressed valuations, and a near-complete shutdown in IPO activity—we view the Janus offering as a notable “green shoot” for the sector. Why this deal matters: A rare bright spot after a difficult cycle. * REITs have spent the past several years in a capital-constrained environment. The fact that this deal is coming to market at all is notable—and potentially signals early-stage normalization. * Potential reopening of the REIT IPO window. If well received, Janus could mark an inflection point for public REIT issuance—particularly for differentiated, asset-backed sectors with visible internal growth. * Private-pay real estate is leading the recovery. Senior housing fundamentals have improved meaningfully: occupancy gains, reaccelerating rent growth, and historically muted new supply. * Demographics are becoming a near-term driver. The Baby Boomer cohort is now entering prime senior housing years, turning a long-dated theme into a tangible earnings driver. On Janus specifically: A rare pure-play SHOP platform. Janus will consist of 34 communities (~10,400 units) carved out of Healthpeak, generating roughly $220M of annual NOI, the vast majority from entrance-fee “Life Plan” communities. What is a CCRC—and how is this different? Much of the portfolio is composed of Continuing Care Retirement Communities (CCRCs)—large, campus-style properties where residents pay a significant upfront entrance fee plus ongoing service fees in exchange for access to a continuum of care.That contrasts with the more common SHOP model (as seen in much of Welltower’s portfolio), which is typically lease-based with no large upfront fee and more direct exposure to rent growth and operating margins. That said, Janus’s portfolio is not a typical CCRC mix, given its heavy weighting toward independent living (typical of the SHOP model). Unlocking value that wasn’t being recognized. Senior housing had become a relatively small and harder-to-value segment within Healthpeak’s broader platform. This separation is a logical step to surface that value. Positioned as a growth platform. Janus is expected to launch with minimal leverage and has an identified ~$675M acquisition pipeline, primarily in rental senior housing. Valuation framework: Janus is targeting up to a $5B valuation, offering 37M shares at $18–$20 to raise roughly $740M. The IPO target (~$5B) implies a ~4.5% cap rate, which would: * Place Janus squarely in line with public REIT valuations, notably Welltower, which trades in the ~4.5%–5.0% implied cap rate range. This aligns with top-tier healthcare REIT multiples, where leading names trade at ~25x P/FFO (a sizable premium to the REIT sector average of around 16-18x) * The $5B valuation is likely at the upper end of the warranted valuation range in the near term, given that CCRC portfolios are not typically assigned the same premium valuation as the SHOP independent living portfolios. Relative to the simplistic “10% of DOC” implied valuation (~$2.2B), even a mid-range IPO outcome suggests substantial value creation through separation and multiple expansion. With minimal initial leverage, Janus would debut as a mid-to-large cap REIT with sufficient scale and float, particularly given DOC’s expected majority ownership but intention to leave meaningful public float. Bottom Line: In our view, Janus represents a convergence of several themes we’ve been highlighting: * Stellar senior housing fundamentals with structurally limited new supply * How some REITs are getting creative to unlock shareholder value amid persistent downward valuation pressures * Early signs that REIT capital markets may be thawing after a prolonged freeze It doesn’t mark the end of the challenges facing REITs, but it may be one of the first clear signals that the cycle is beginning to turn.

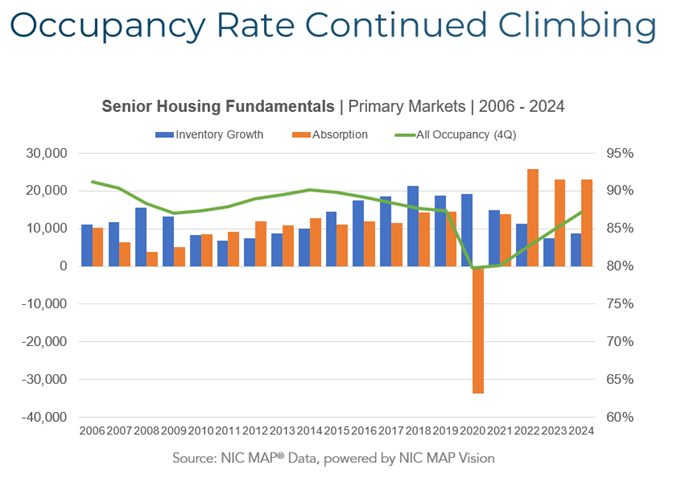

Infographic showing U.S. senior housing fundamentals in primary markets (2006–2024): occupancy continued climbing through Q4 2024 as net absorption outpaced muted inventory growth. This directly supports the point that private-pay senior housing fundamentals are strengthening ahead of the Janus Living IPO and a potential thaw in REIT capital markets.

Source: National Investment Center for Seniors Housing & Care (NIC)

Research Brief

What our analysis found

Healthpeak Properties announced on January 7, 2026, the formation and planned IPO of Janus Living (NYSE: JAN), a pure-play senior housing REIT structured under the RIDEA (SHOP) model. The company will comprise 34 senior housing communities totaling 10,422 units, carved out of Healthpeak's existing portfolio, with an annualized cash NOI of approximately $220 million. The portfolio is heavily weighted toward independent living at 69% of units, with assisted living, memory care, and skilled nursing comprising the remainder. Key markets include Tampa (20%), Houston (19%), Philadelphia (9%), and Orlando (9%). BofA Securities and J.P. Morgan are serving as lead bookrunners, and the S-11 registration statement was publicly filed on February 27, 2026.

The deal arrives at a pivotal moment for REIT capital markets. S&P Global reports only three US equity REIT IPOs in 2025, down from six in 2024, underscoring the near-frozen state of public REIT issuance. Yet underlying senior housing fundamentals have strengthened considerably: NIC MAP Vision data shows US senior housing occupancy reached 89.1% at year-end 2025, marking 18 consecutive quarters of improvement, while asking-rent growth ran at roughly 4.3% year-over-year and new construction remained at or near record lows. Janus is targeting a valuation of up to $5 billion, offering 37 million shares at $18–$20 per share to raise approximately $740 million, implying a cap rate of roughly 4.5% in line with top-tier healthcare REIT multiples.

Demographics lend further urgency to the thesis. Pew Research Center notes the oldest Baby Boomers turn 80 in 2026, shifting what was a long-dated demographic tailwind into a near-term demand catalyst for senior housing. Janus will launch with minimal leverage, targeting opening Net Debt/Adjusted EBITDA below 1x, and has an identified acquisition pipeline of approximately $675 million in rental senior housing assets under signed LOIs or purchase agreements. Healthpeak will retain a substantial majority interest and externally manage Janus through an affiliate for an annual fee of roughly $10 million.

Fact Check

Evidence from both sides

Supporting Evidence

REIT IPO market has been largely frozen

S&P Global confirmed only three US equity REIT IPOs debuted on the NYSE or Nasdaq in 2025, down from six in 2024, validating the tweet's characterization of a "near-complete shutdown in IPO activity" and the significance of Janus coming to market (spglobal.com, January 2026).

Senior housing occupancy has risen for 18 consecutive quarters

NIC MAP Vision reported US senior housing occupancy reached 89.1% at the end of 2025, the 18th straight quarterly gain, directly supporting the tweet's claim that "occupancy gains" are driving improved fundamentals (newslink.mba.org, January 2026).

Rent growth reaccelerating amid historically low new supply

Third-quarter 2025 asking-rent growth of approximately 4.3% year-over-year and construction starts at or near record lows confirm the tweet's assertion of "reaccelerating rent growth" and "historically muted new supply" (NIC MAP Vision data via MBA Newslink).

Baby Boomers entering prime senior housing years is now a near-term catalyst

Pew Research Center documented that the oldest Baby Boomers turn 80 in 2026, and Brookings similarly highlighted this demographic milestone, corroborating the tweet's claim that demographics are shifting from a long-dated theme to a tangible earnings driver (pewresearch.org, January 2026).

Janus is a 100% RIDEA pure-play SHOP platform with heavy IL weighting

Healthpeak's investor presentations confirm the portfolio operates entirely under the RIDEA structure with 69% independent living units, consistent with the tweet's description of a "rare pure-play SHOP platform" with atypical CCRC mix (Healthpeak December 2025 and February 2026 presentations).

Minimal opening leverage and identified acquisition pipeline

Healthpeak disclosed a target opening Net Debt/Adjusted EBITDA of less than 1x and approximately $675 million in senior housing investments under signed LOIs or purchase agreements, supporting the tweet's characterization of Janus as a growth platform with balance sheet flexibility (nasdaq.com, Senior Housing News).

Portfolio scale and NOI align with tweet's figures

Healthpeak's December 2025 presentation shows annualized cash NOI of $220 million and the 34-community, 10,422-unit portfolio matches the tweet's stated metrics precisely (Healthpeak investor presentations via s202.q4cdn.com).

Broader REIT capital markets showing signs of thawing

Nareit data shows REITs raised $80 billion through capital offerings in 2025, indicating improved access to capital even as IPO activity specifically remained subdued, lending partial support to the tweet's "early signs of thawing" thesis (spglobal.com).

Contradicting Evidence

External management structure introduces conflicts and fee drag

The tweet does not mention that Janus will be externally managed by a Healthpeak affiliate under an Exclusivity Agreement, with an annual management fee of approximately $10 million. External management structures are typically viewed negatively by REIT investors due to potential conflicts of interest, fee leakage, and misalignment of incentives, which could weigh on Janus's valuation relative to internally managed peers like Welltower (SEC filings, nasdaq.com).

The $5 billion target valuation may be aggressive given CCRC portfolio composition

The tweet itself acknowledges that "CCRC portfolios are not typically assigned the same premium valuation as the SHOP independent living portfolios," yet the targeted ~4.5% cap rate would place Janus in line with Welltower, which operates a more conventional and diversified SHOP model. A Mizuho note cited by Senior Housing News suggests Welltower's implied cap rate is closer to 4%, meaning Janus would need to justify near-peer pricing despite a fundamentally different and historically lower-valued entrance-fee model.

NOI figures require nuance around entrance-fee accounting

Healthpeak's February 2026 presentation shows 2025 Adjusted NOI of only $197 million, with the $220 million headline figure requiring the addition of $54 million in non-refundable entrance-fee cash above GAAP amortization. This accounting treatment inflates the apparent income stream and may not be directly comparable to conventional SHOP NOI, potentially making the implied cap rate appear more favorable than underlying recurring economics warrant (Healthpeak February 2026 presentation).

Three REIT IPOs in 2025 does not necessarily signal a reopening window

While the tweet frames Janus as a potential inflection point for REIT IPO activity, the decline from six IPOs in 2024 to three in 2025 actually represents a worsening trend, not improvement. A single additional IPO in 2026 may simply reflect one company's idiosyncratic circumstances rather than a broader market reopening (spglobal.com).

Healthpeak retaining majority ownership limits true public float

The tweet notes Healthpeak's intention to maintain majority ownership, which could constrain Janus's public float, limit index inclusion prospects, and reduce secondary market liquidity—factors that often result in a trading discount rather than the premium valuation the IPO pricing implies (ir.healthpeak.com).

Geographic concentration poses risk

Nearly 40% of Janus's units are concentrated in just two markets—Tampa (20%) and Houston (19%)—exposing the portfolio to regional economic, regulatory, and weather-related risks that are not addressed in the tweet's broadly optimistic framing (Healthpeak February 2026 presentation).

Senior housing occupancy remains below pre-pandemic levels

While 89.1% occupancy represents 18 quarters of improvement, it still falls short of the approximately 90%+ occupancy rates that prevailed before COVID-19 disrupted the sector, suggesting the recovery narrative, while valid, is incomplete (NIC MAP Vision data).

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.