Kevin O'Leary says you can become a millionaire on $69,000 a year. “Take 20% of your salary of $69,000 and put it into the market each week and don't touch it” https://t.co/zmaQHNI8LE

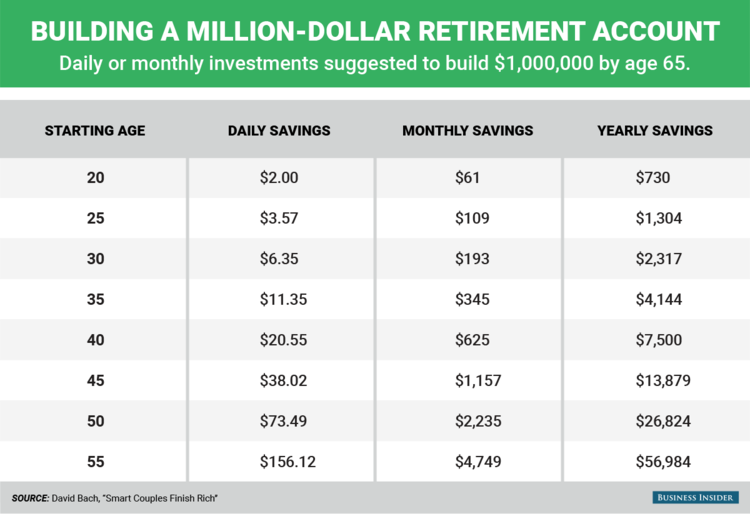

A table-style infographic (originally from David Bach and reproduced by Business Insider) that lists the daily, monthly and yearly savings required to build $1,000,000 by age 65 (the chart assumes Bach’s investment-return assumptions). It’s directly relevant because the chart shows a yearly savings need of about $13,879 for someone starting at age 45 — nearly the same as 20% of a $69,000 salary (~$13,800) — illustrating the scenario Kevin O’Leary described under the chart’s assumptions.

Source: Business Insider / David Bach

Research Brief

What our analysis found

Kevin O'Leary, the well-known investor and Shark Tank star, sparked widespread debate after appearing on The Iced Coffee Hour podcast on March 29, 2026, where he declared that anyone earning $69,000 a year can become a millionaire by investing 20% of their salary into the stock market each week and never touching it. That translates to roughly $13,800 per year, or about $265 per week, funneled into broad-market equities over a multi-decade horizon.

The advice quickly went viral, with outlets like AOL, Benzinga, and Fortune publishing breakdowns of the math. Using commonly cited long-run U.S. stock returns of 8–10% annually, published calculations showed the strategy could yield roughly $1.1 million in 25 years at 8% or as much as $4.4 million over 35 years at 10%. The arithmetic of compound interest undeniably supports the possibility — on paper.

However, critics were swift to point out that the advice glosses over major real-world barriers. The U.S. personal saving rate stood at just 3.6% in late 2025, according to the Bureau of Economic Analysis, and Vanguard's "How America Saves" report shows average employee 401(k) deferral rates hovering around 7–8% — far below O'Leary's 20% target. With U.S. Census data placing median full-time individual earnings near $63,360, many workers earn less than $69,000, and those who do often face housing, healthcare, and childcare costs that make saving a fifth of gross income extraordinarily difficult.

Fact Check

Evidence from both sides

Supporting Evidence

The compound-interest math checks out

At a 10% annualized return, investing $13,800 per year for 30 years yields approximately $2.6 million, and at 8% over 25 years the total reaches roughly $1.1 million, according to calculations published by AOL and Benzinga in early April 2026. The raw arithmetic confirms that consistent contributions at historical market return rates can produce seven-figure outcomes.

Historical stock returns support the assumed growth rate

Long-run U.S. large-cap equity total returns have averaged roughly 9–11% nominally over periods stretching back to 1926, a range cited by financial historians and referenced in Washington Post and other reporting. O'Leary's implicit return assumptions fall within this well-documented historical band.

The salary figure is within reach for many American workers

U.S. Census data show median earnings for full-time, year-round workers at approximately $63,360, and median household income between $82,000 and $84,000 in 2023–2024. A $69,000 individual salary, while above the individual median, is attainable for a significant portion of the workforce and is below the household median.

Dollar-cost averaging is a widely endorsed strategy

O'Leary's instruction to invest a fixed amount "each week" and "don't touch it" aligns with the broadly recommended practice of dollar-cost averaging into low-cost index funds, a strategy endorsed by investment firms and financial planners as a way to smooth out market volatility over long time horizons.

Contradicting Evidence

It takes roughly 30 years, not a quick path

Tech investor Adam Cochran and other commentators noted that even with perfect discipline, the strategy requires approximately 30 years to reach $1 million at moderate return assumptions — and that calculation excludes the drag of taxes on gains. For many workers starting in their 30s or 40s, this timeline may extend past traditional retirement age.

Almost no one actually saves 20% of gross income

The Bureau of Economic Analysis reported a national personal saving rate of just 3.6% in late 2025, and Vanguard's retirement data show median employee 401(k) deferral rates around 7–8%, with combined employer-plus-employee contributions averaging only about 11–12%. A 20% gross savings rate is far beyond what the vast majority of American workers currently achieve.

After-tax income makes the math much harder

O'Leary frames the target as 20% of a $69,000 gross salary, but federal and state income taxes, plus payroll taxes, can reduce take-home pay to roughly $50,000–$55,000 depending on location. Setting aside $13,800 from that net figure means dedicating approximately 25–28% of actual take-home pay, a far steeper burden than the headline number suggests.

Living costs make it infeasible for many households

Fortune and other outlets noted that high housing, healthcare, and childcare expenses consume the bulk of income for many American families, especially in costly metro areas. Census data confirm wide regional income variation, and workers earning at or below the $63,360 median may have virtually no margin for a 20% savings rate after essential expenses.

The projection ignores inflation

The million-dollar milestone sounds impressive in today's terms, but at a 3% average inflation rate over 30 years, $1 million in future dollars would have the purchasing power of roughly $400,000–$412,000 today — a comfortable nest egg but far from the aspirational wealth the headline implies.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.