In a sudden turn of events, US 12-month inflation expectations have surged to 5.2%, the highest level since March 2023. In just 3 weeks, markets have gone from pricing-in rate cuts to rate hikes. https://t.co/jphiqMwniL

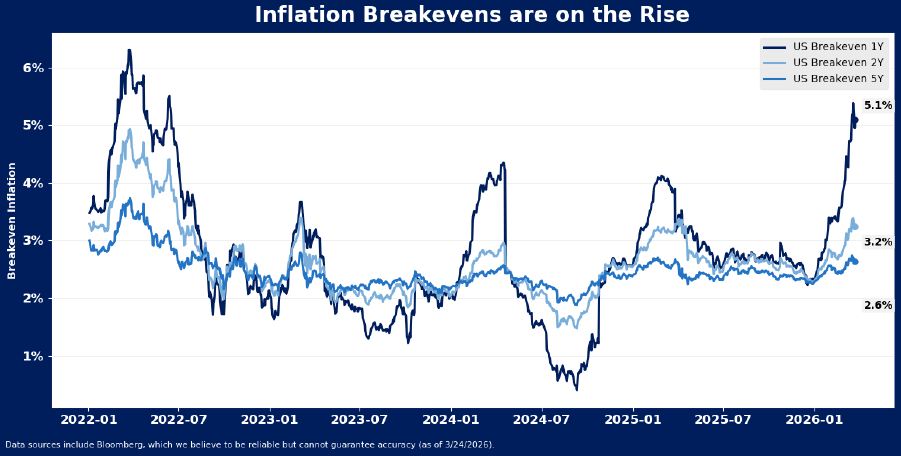

Line-chart infographic (data through March 24, 2026) showing US breakeven inflation rates (1Y, 2Y, 5Y). The 1‑year breakeven spikes to about 5.1%, visually illustrating the sharp rise in 12‑month market‑based inflation expectations and supporting the tweet’s point that markets quickly re‑priced from cuts toward potential rate hikes.

Source: HB Wealth

Research Brief

What our analysis found

On March 20, 2026, the U.S. 1-year market-implied breakeven inflation rate surged to approximately 5.2–5.3%, its highest reading since March 2023, according to Bloomberg terminal data (USGGBE01) widely cited by market reporters and financial commentators. The spike was driven primarily by a sharp rally in crude oil prices — Brent crude traded above $108–$112 per barrel in the March 18–22 window — triggered by escalating tensions and supply disruptions around the Strait of Hormuz involving Iran. The energy shock rippled through short-dated inflation pricing and prompted a dramatic reassessment of Federal Reserve policy expectations, with fed-funds futures shifting from pricing in rate cuts to assigning meaningful odds of rate hikes within a matter of weeks.

The Federal Reserve, at its March 17–18 FOMC meeting, held the policy rate steady at 3.50–3.75% but revised its 2026 core PCE inflation projection upward to roughly 2.7% in the Summary of Economic Projections. Meanwhile, the OECD's March 2026 Interim Economic Outlook raised its U.S. all-items inflation forecast for the year to approximately 4.2%, and the Conference Board's March consumer confidence survey explicitly noted a "surge" in household inflation expectations tied to oil and geopolitical factors.

However, important caveats temper the alarm. Consumer survey measures told a materially different story: the University of Michigan's final March reading placed year-ahead inflation expectations at only ~3.4%, and the New York Fed's Survey of Consumer Expectations landed in a similar mid-3% range — well below the 5.2% breakeven figure. Longer-horizon breakevens (5-year and 10-year rates remained at roughly 2.3–2.7%) showed no evidence of broad inflation de-anchoring, and Federal Reserve research has long cautioned that TIPS-based breakevens embed risk premia and liquidity effects that can amplify short-term moves beyond true expected inflation.

Fact Check

Evidence from both sides

Supporting Evidence

Bloomberg 1-year breakeven data confirms the 5.2% figure

Bloomberg terminal snapshots (USGGBE

circulated on March 20, 2026 showed the 1-year market-implied breakeven inflation rate spiking to approximately 5.2–5.3%, consistent with the tweet's claim

The reading was widely reported by Bloomberg journalists and embedded in financial blogs such as A Wealth of Common Sense.

Oil shock provided a clear fundamental catalyst

Brent crude surged above $108–$112 per barrel during the March 18–22 window due to Iran-related disruptions near the Strait of Hormuz, as reported by The Guardian. Energy pass-through to headline inflation expectations explains the sharp lift in short-dated breakevens.

Fed-funds futures repriced rapidly toward hikes

Fortune and other financial outlets reported on March 20, 2026 that markets shifted from pricing in rate cuts to assigning non-zero probabilities of rate hikes, with investment bank Macquarie explicitly calling for a potential hike, corroborating the tweet's claim of a dramatic policy-expectation reversal.

Official bodies raised U.S. inflation projections

Both the Fed's March SEP (core PCE revised up to ~2.7% for

and the OECD's March 2026 Interim Economic Outlook (U.S. all-items inflation rai...

and the OECD's March 2026 Interim Economic Outlook (U.S. all-items inflation raised to ~4.2%) reflected a genuine upward shift in near-term inflation risk, lending institutional weight to the market signal.

Consumer surveys corroborated rising expectations directionally

The Conference Board's March 2026 consumer confidence release explicitly noted that 12-month inflation expectations "surged," attributing the move to oil prices and geopolitical conflict, supporting the narrative of a broad inflation-expectations shock.

Contradicting Evidence

Consumer survey measures were far below 5.2%

The University of Michigan's final March 2026 consumer sentiment release reported year-ahead inflation expectations of approximately 3.4%, and the New York Fed's Survey of Consumer Expectations showed a similar mid-3% reading. These widely followed household surveys suggest the 5.2% market-implied figure significantly overstates what consumers actually expected for inflation.

Longer-term breakevens showed no de-anchoring

Five-year and 10-year breakeven inflation rates remained in the 2.3–2.7% range in late March 2026, indicating the spike was concentrated exclusively at the very short end of the curve rather than reflecting a fundamental re-anchoring of inflation expectations — an important distinction the tweet does not convey.

TIPS breakevens are not pure inflation expectations

Federal Reserve research has repeatedly emphasized that breakeven rates incorporate an inflation-risk premium and are subject to liquidity and technical distortions, especially at very short maturities. A sudden spike in 1-year breakevens can reflect transient energy-price shocks and risk-premium surges rather than a durable change in underlying inflation expectations.

The tweet conflates a market-implied measure with broad "inflation expectations"

Describing the 1-year breakeven as "US 12-month inflation expectations" without qualification is misleading. It is one market-based gauge, not a consensus economic forecast or a survey-based expectation, and its March 2026 reading diverged sharply from other standard measures of inflation expectations.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.