BREAKING: Markets are now fully pricing-in two 25 basis point rate HIKES by the European Central Bank in 2026.

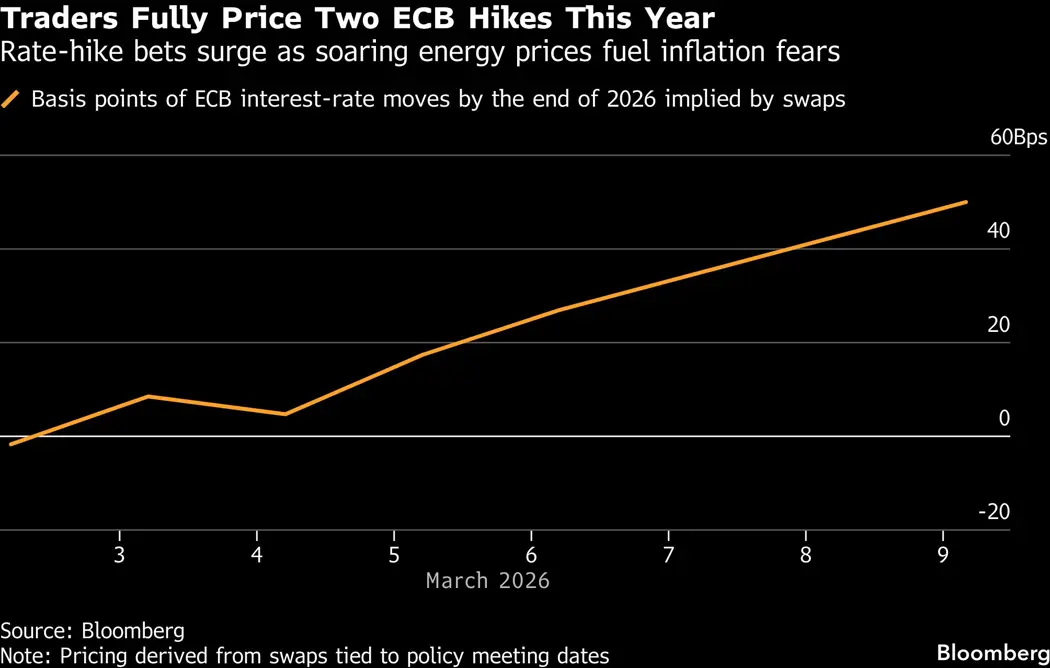

A Bloomberg chart showing swaps-implied cumulative ECB rate moves by the end of 2026, which climb to roughly 50 basis points as of early March 2026. This visual directly illustrates markets fully pricing in two 25 bp ECB hikes in 2026.

Source: Energy Connects (via Bloomberg)

Research Brief

What our analysis found

A dramatic repricing of European Central Bank rate expectations swept through bond markets in early March 2026, triggered by an oil price shock stemming from the Iran conflict and disruptions to the Strait of Hormuz. On March 9, 2026, Brent crude briefly surged toward $119–$120 per barrel, prompting a global bond selloff and a sharp reassessment of the ECB's policy path. Just weeks earlier, the ECB's own Economic Bulletin, published on January 15, 2026, had noted that markets expected no policy rate changes in either direction for the entire year.

The speed of the repricing was remarkable. Euro short-term rate (€STR) overnight index swap markets briefly moved to price in two full 25-basis-point rate hikes by the ECB before year-end on March 9, with one source noting 40 basis points of cumulative hikes were embedded in the curve intraday. Germany's benchmark 10-year Bund yield climbed to 2.963% on March 12 — its highest level since October 2023 — reflecting the inflation anxiety coursing through European fixed income.

However, the "two full hikes" pricing proved fleeting. By March 11–12, money markets had settled on one hike fully priced by July and only a 70–85% probability of a second hike by December. Large European institutional investors publicly called the swings excessive. As of mid-March, further geopolitical escalation — including reports of an attack on Iran's South Pars gas field — kept oil elevated and inflation fears alive, but confirmation that markets had returned to fully pricing two hikes remained elusive.

Fact Check

Evidence from both sides

Supporting Evidence

Reuters and Bloomberg confirmed two-hike pricing on March 9

A Reuters piece syndicated on Investing.com reported that "investors moved to price in two rate hikes from the European Central Bank by year-end" as bonds plunged on the oil spike. Separately, Bloomberg via EnergyConnects stated that "swaps imply two full 25-basis-point hikes by the ECB this year compared with one on Friday."

OCBC quantified roughly 40 bps of hikes priced

An OCBC rates strategy note published on March 9 stated that EUR OIS markets had priced 40 basis points of hikes for 2026, consistent with approximately 1.5 to 2 quarter-point increases being embedded in the curve.

Alliance News headline explicitly cited two ECB hikes

A MarketScreener/Alliance News headline on March 9 directly stated that "money markets price in two ECB hikes," capturing the intraday state of swap market pricing.

A clear catalyst existed in the oil shock

Brent crude surged over 25% toward $119–$120 per barrel on March 9 due to the escalating Iran conflict and Strait of Hormuz disruptions, providing a tangible inflationary impulse that justified the hawkish repricing.

Contradicting Evidence

Two-hike pricing was brief and faded the same day

Later on March 9 itself, a Reuters wrap reported traders "fully price one quarter-point hike in 2026, with around a 25% chance of a second," showing the two-hike pricing was an intraday extreme rather than a settled market consensus.

By March 11–12, markets priced only one full hike plus a partial second

Reuters reported on March 12 that money markets were "fully pricing an ECB rate hike by July, and a 70% chance of a second increase by December" — later updated to about 85% — meaning two hikes were never durably "fully priced in."

Major investors called the repricing excessive

On March 10, Reuters quoted large European investors saying the rate swings "have gone too far," explicitly noting that traders had "priced as many as two 2026 rate hikes from the ECB on Monday" only briefly before retracing.

The baseline before the shock was zero rate changes

The ECB's Economic Bulletin from January 15, 2026 stated that the €STR forward curve "indicated that markets were not expecting any policy rate changes in either direction this year," underscoring how exceptional and potentially transitory the two-hike pricing was.

The tweet's use of "now" and "fully" overstates the durability

While markets did briefly touch two-hike pricing on March 9, the word "fully" implies a settled, sustained market expectation, which multiple subsequent data points contradict — pricing fluctuated significantly even within individual trading sessions.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.