🚨 BREAKING FED WILL INJECT $40,462,000,000.00 INTO THE MARKETS OVER THE NEXT FEW WEEKS! THEY'RE OFFICIALLY CONTINUING QE AND TURNING THE MONEY PRINTER BACK ON! GIGA BULLISH FOR MARKETS! https://t.co/6W0sBgLncA

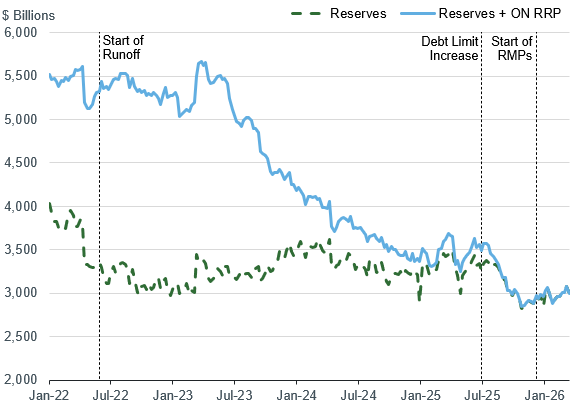

Line chart showing the level of bank reserves (and reserves plus ON RRP) from Jan‑2022 to Jan‑2026 with vertical markers for 'Start of Runoff', 'Debt Limit Increase' and 'Start of RMPs' — it directly illustrates the Fed's reserve decline and the timing of reserve management purchases (the ~$40B/month program) that represent the liquidity injections referenced in the tweet.

Source: Federal Reserve Bank of New York (The Teller Window)

Research Brief

What our analysis found

The tweet references a real Federal Reserve program. On December 10, 2025, the FOMC directed the New York Fed's Open Market Trading Desk to begin reserve management purchases (RMPs) — secondary-market purchases of short-dated Treasury securities designed to keep reserve balances "ample." The first monthly schedule was released on December 11, 2025, with purchases commencing December 12, 2025 at a pace of roughly $40 billion per month. The tweet's figure of $40,462,000,000 aligns closely with the Desk's published operational details, which show planned RMP amounts of approximately $40 billion for several monthly periods, alongside separate reinvestment purchases that can push total monthly buying above $50 billion.

However, the tweet's characterization of this activity as the Fed "officially continuing QE" and "turning the money printer back on" is strongly disputed by the Fed itself. Vice Chair Philip Jefferson and New York Fed officials have explicitly stated that RMPs are not quantitative easing — they are operational measures to manage reserve levels, not a shift in monetary policy stance. Moreover, the monthly RMP pace is not fixed: the April 14–May 13, 2026 schedule, for instance, showed a reduced plan of approximately $25 billion, down from the $40 billion seen in prior periods. This variability undermines the claim that the Fed has permanently restarted large-scale asset purchases.

Fact Check

Evidence from both sides

Supporting Evidence

The $40 billion figure matches official Fed schedules

The New York Fed's Statement Regarding Reserve Management Purchases Operations, dated December 10, 2025, directed the Desk to purchase approximately $40 billion in short-dated Treasuries in its first monthly schedule, with purchases beginning December 12, 2025. The tweet's $40.462 billion figure is consistent with these published operational details (source: newyorkfed.org).

Published Desk schedules confirm ongoing monthly purchases

The NY Fed's Treasury Securities Operational Details page lists multiple monthly periods with RMP targets near $40 billion — for example, the March 13–April 13, 2026 period planned approximately $40.0 billion in RMPs plus $13.8 billion in reinvestment purchases, confirming sustained buying activity over consecutive months (source: newyorkfed.org).

Independent market participants corroborated the program's scale

The Federal Home Loan Bank of New York's weekly market update on December 12, 2025 noted the Fed's new RMP program would buy T-bills "to the tune of $40 billion per month," citing specific scheduled purchases such as an $8.167 billion operation on December 12 (source: fhlbny.com).

The purchases do add reserves to the banking system

Because the Desk is buying Treasury securities in the secondary market and crediting dealer accounts, the operations mechanically increase reserve balances in the financial system, which is the factual kernel behind the tweet's claim of "injecting" money into markets.

Contradicting Evidence

The Fed explicitly says this is not quantitative easing

Vice Chair Philip Jefferson and New York Fed officials have stated on the record that reserve management purchases are operational tools to maintain ample reserves — not a policy shift to QE. The Desk's own documentation frames RMPs as distinct from the large-scale asset purchase programs used during economic crises (source: federalreserve.gov, remarks dated January 16, 2026).

The monthly purchase pace is not fixed and has already declined

The tweet implies a permanent restart of massive buying, but the RMP amount changes month to month based on reserve conditions. The April 14–May 13, 2026 schedule showed planned RMPs of only approximately $25 billion, a significant reduction from the $40 billion pace in earlier periods. Future amounts are announced monthly and can be adjusted in either direction (source: newyorkfed.org).

Purchases target only short-dated securities, unlike crisis-era QE

RMPs are limited to Treasury bills and, if necessary, coupon securities with three years or less remaining maturity. Traditional QE involved purchases across the yield curve, including long-dated bonds and mortgage-backed securities, with the explicit goal of easing financial conditions. The narrow focus of RMPs is designed to minimize market impact, not stimulate the economy.

Calling it "GIGA BULLISH" overstates the market implications

Because the Fed is buying short-duration instruments for reserve-management purposes — not signaling easier monetary policy — most economists and Fed watchers caution against interpreting RMPs as a catalyst for risk-asset rallies in the way that traditional QE programs historically were.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.