SUMMARY OF FED DECISION (3/18/2026): 1. Fed halts rate cuts for the second straight meeting 2. Fed projects one rate cut in 2026, one in 2027 3. Fed 2026 PCE inflation forecast revised higher to 2.7% 4. Fed says implications of Middle East developments are "uncertain" 5. Fed Governor Miran dissents in favor of an interest rate cut 6. Today's rate decision was reached in an 11-1 vote We believe December was Fed Chair Powell's final rate cut.

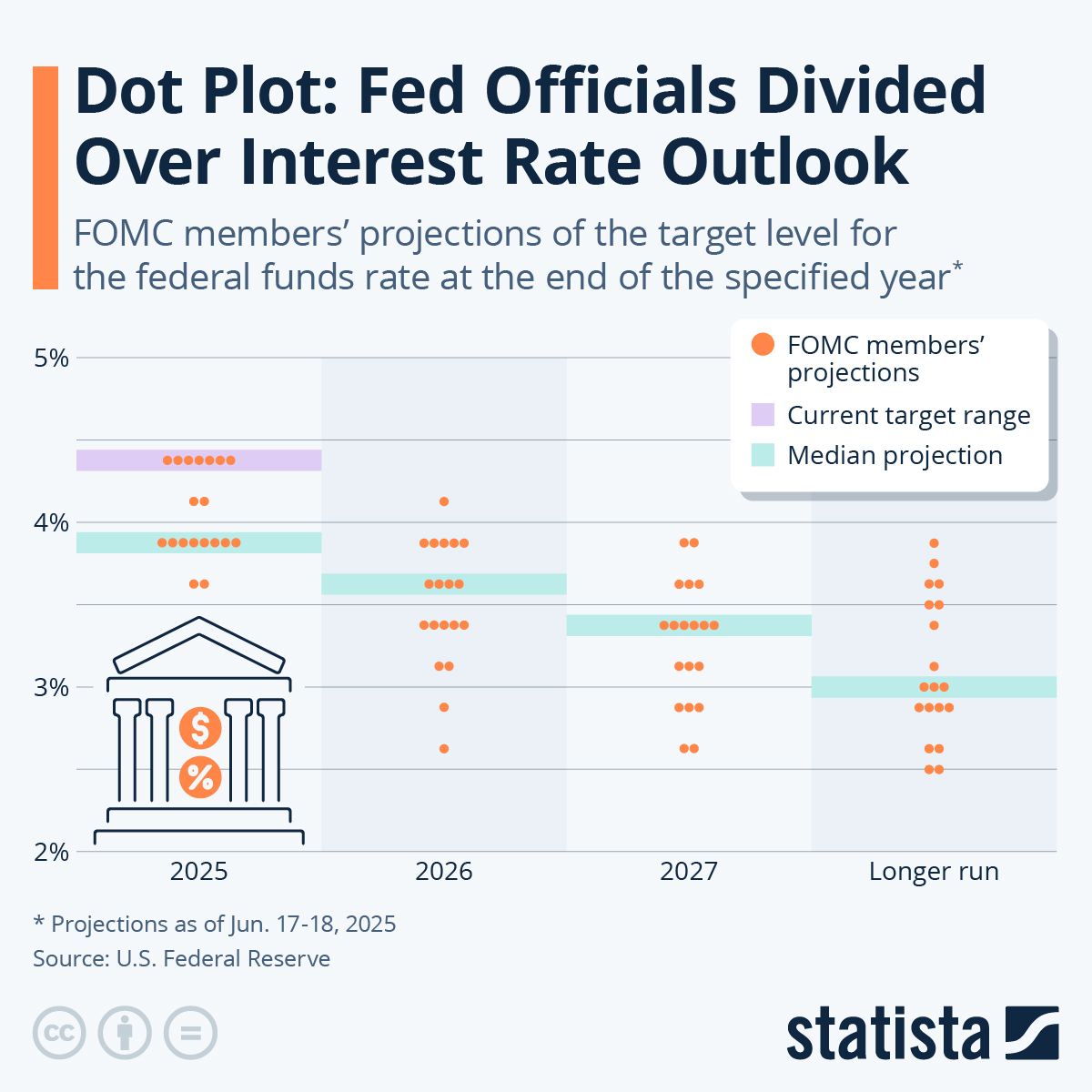

This Statista infographic visualizes the FOMC "dot plot" (projections as of Dec. 9–10, 2025), charting policymakers’ expected federal funds rate path through 2027. It highlights the shallow easing path with only limited cuts in 2026–27, aligning with the tweet’s point about one cut in 2026 and one in 2027.

Source: Statista

Research Brief

What our analysis found

The Federal Reserve on March 18, 2026, held its benchmark fed-funds rate steady at 3.50%–3.75% for the second consecutive meeting, following an identical pause at the January 28 meeting. The decision was approved on an 11–1 vote, with Governor Stephen Miran casting the lone dissent in favor of a 25 basis-point cut. In its post-meeting statement, the FOMC flagged that the implications of escalating Middle East developments for the U.S. economy remain "uncertain", a notable addition reflecting the ongoing Iran conflict and its ripple effects through energy markets.

The economic backdrop heading into the decision was marked by conflicting signals. The labor market showed clear signs of cooling, with February nonfarm payrolls contracting by −92,000 jobs and the unemployment rate ticking up to 4.4%. At the same time, inflationary pressures intensified as Brent crude surged above $109 per barrel amid disruptions near the Strait of Hormuz, fueling fears of an energy-driven price spike. The January Producer Price Index had already shown a hot +0.5% month-over-month gain, reinforcing the Fed's cautious stance.

The updated Summary of Economic Projections reportedly shows the median FOMC participant expecting just one rate cut in 2026 and one in 2027, a shallow easing path that has persisted since mid-2025. However, the distribution of views is wide: Fortune reports that 7 of 19 officials see no cuts at all this year, while others project more aggressive easing. The tweet's claim that the 2026 PCE inflation forecast was revised up to 2.7% remains unverified, as the official March SEP tables had not yet been published at the time of reporting, though such a revision would be directionally consistent with the oil-price shock and sticky inflation readings.

Fact Check

Evidence from both sides

Supporting Evidence

Fed holds rates for a second straight meeting

Fortune's March 18 report confirms the FOMC left the target range at 3.50%–3.75%, matching the January 28 hold, making this the second consecutive pause after a string of late-2025 cuts.

11–1 vote with Governor Miran dissenting

Fortune describes the decision as "nearly unanimous, save for Stephen Miran," who favored a quarter-point cut. Wikipedia's FOMC actions log corroborates the 11–1 tally.

Statement references Middle East uncertainty

Fortune directly quotes the FOMC statement as saying the implications of Middle East developments for the U.S. economy are "uncertain," consistent with the tweet's characterization.

Dot plot shows one cut in 2026, one in 2027

Coverage from the September 2025 and December 2025 SEP releases showed the median participant projecting roughly one cut each in 2026 and 2027, and early reporting on the March 2026 release indicates that restrained outlook has persisted.

Miran's dovish dissent is part of a pattern

January 2026 FOMC minutes published by the Federal Reserve show both Miran and Governor Waller dissented for a cut at the prior meeting, establishing a track record of internal pressure for easing that carried into March.

Geopolitical and energy backdrop aligns with cautious tone

Brent crude breached $100 in the days before the meeting and topped $109 on decision day, while February payrolls fell by 92,000 — conditions that support the Fed's stated uncertainty about the economic outlook.

Contradicting Evidence

2026 PCE inflation forecast of 2.7% is unverified

The Fed's official March 2026 Summary of Economic Projections had not been posted on the Board of Governors' website at the time of the tweet, and no major wire service had published the full projection table. Prior official SEPs placed 2026 PCE inflation at roughly 2.2%–2.4%, so while a jump to 2.7% is plausible given the oil shock, it cannot yet be confirmed against primary sources.

"One cut in 2026" oversimplifies a divided committee

Fortune reports that 7 of 19 FOMC participants see no rate cuts at all in 2026, while others project more than one. Describing the outlook as "one cut" reflects only the median dot and masks significant disagreement within the committee about the appropriate path.

"December was Powell's final rate cut" is opinion, not fact

This is an editorial judgment by the tweet's author, not a conclusion drawn from the Fed's statement or projections. Goldman Sachs, for instance, delayed but did not abandon its forecast for a 2026 rate cut, citing evolving inflation risks from the Middle East conflict. Multiple Wall Street firms still see a plausible path to at least one cut later this year if energy prices stabilize and labor market weakness deepens.

Miran's title is "Governor," not a special designation

While a minor point, describing Miran simply as "Fed Governor" is accurate but omits that he also dissented at the January meeting alongside Governor Waller, who did not dissent in March — a shift that suggests the internal debate is evolving and the hawkish consensus may be less stable than the 11–1 vote implies.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.