Many fund managers and 'experts' are talking nonsense when they claim FIIs are selling just because Indian markets are 'expensive.' The truth is in the timeline: they’ve been selling since 2018, the moment the government introduced LTCG and hiked STT. Look at the data—in 2021 and 2022 alone, they dumped ₹3.5 lakh crore. This isn't a valuation issue; it's a policy issue.

Source: Mint (livemint.com)

Research Brief

What our analysis found

A viral tweet claims that Foreign Portfolio Investors (FPIs) have been continuously selling Indian equities since 2018, driven primarily by the reintroduction of Long-Term Capital Gains (LTCG) tax and successive hikes in the Securities Transaction Tax (STT), rather than by valuation concerns. The tweet further asserts that FPIs dumped ₹3.5 lakh crore in 2021 and 2022 alone. While the policy grievance has genuine roots—LTCG at 10% on gains above ₹1 lakh was reintroduced in the Union Budget 2018, and STT on options was raised from 0.05% to 0.0625% in 2023 and further to 0.1% in 2024—the actual flow data tells a far more complicated story.

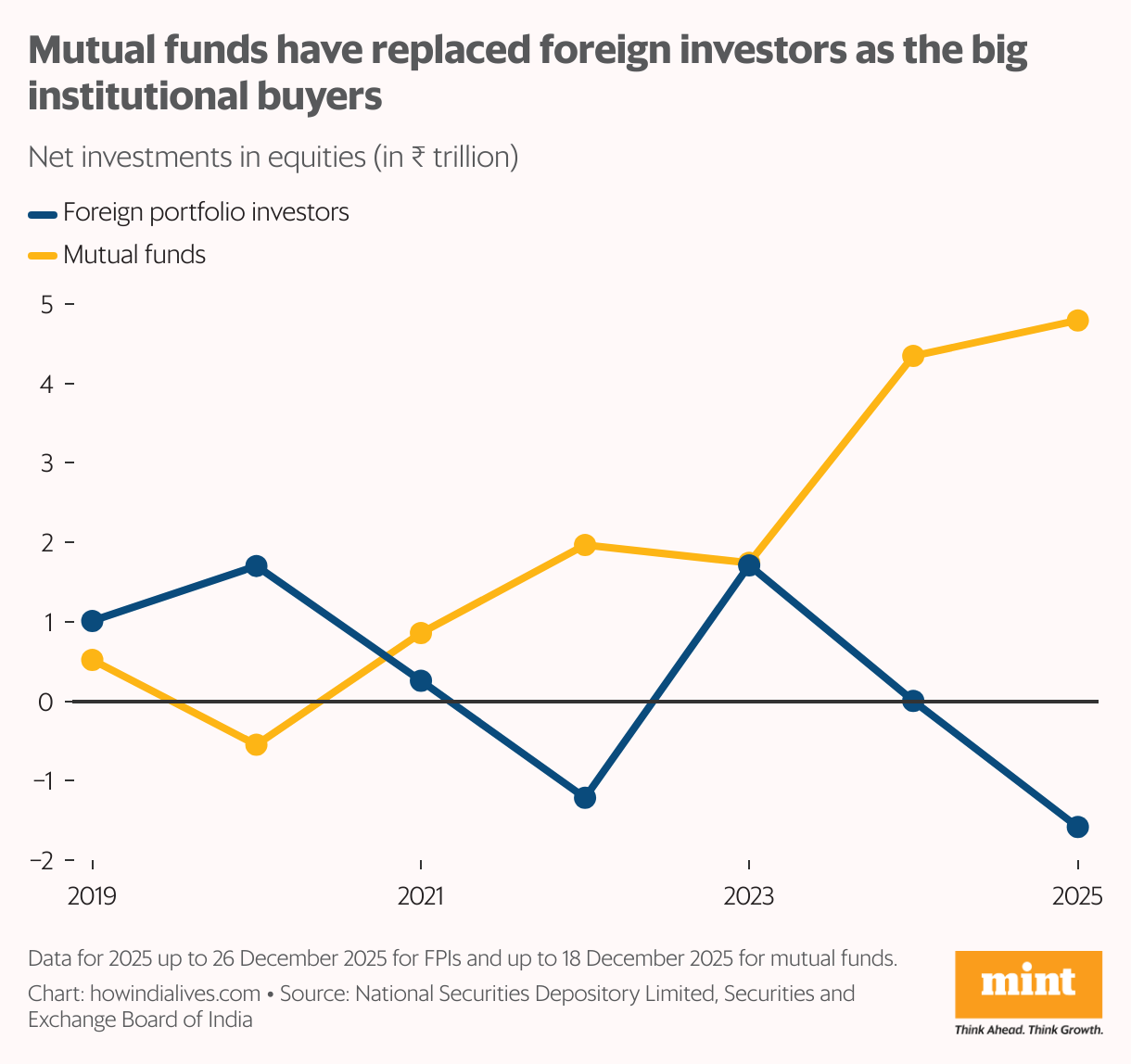

NSDL-based tallies show that after a net outflow of approximately ₹33,000–34,100 crore in 2018, FPIs returned as strong net buyers in subsequent years: ₹1.01 lakh crore in 2019, ₹1.70 lakh crore in 2020, and roughly ₹25,752 crore in 2021. The heaviest single-year selling came in 2022, at about ₹1.21 lakh crore in equities, but this was followed by a massive reversal in 2023, when FPIs poured in approximately ₹1.71 lakh crore—one of the highest annual inflows on record. The claim that ₹3.5 lakh crore was pulled out across 2021 and 2022 is not supported by the data; 2021 was in fact a year of modest net inflows, and 2022's outflows were around ₹1.21 lakh crore.

Analysts and industry bodies have indeed flagged India's layered tax structure—including LTCG, STT, and surcharges—as persistent "irritants" that reduce post-tax returns for foreign investors. The Budget 2026 proposal to raise STT on options to 0.15% and futures to 0.05% from April 2026 triggered an immediate market sell-off. However, multiple experts attribute the large 2022 and 2025 outflows primarily to global factors: U.S. Federal Reserve rate hikes, a surging dollar, and elevated Indian equity valuations relative to peers such as China, which staged a sharp rally in late 2024. The reality, therefore, is far more nuanced than a single-cause policy narrative.

Fact Check

Evidence from both sides

Supporting Evidence

2018 outflows coincided with LTCG reintroduction

FPIs pulled out approximately ₹33,000–34,100 crore in 2018, the first calendar-year net selling since 2011, shortly after the 10% LTCG tax was announced in Budget 2018. Media reports and op-eds attributed part of the exodus to the new tax, according to Indian Express and Business Today.

Sharp Q2 2018 selling linked to tax policy

In just April–June 2018, FPI equity outflows totaled roughly ₹61,132 crore, with coverage citing the newly introduced LTCG tax as a contributing factor, per Business Today.

Industry has repeatedly flagged tax irritants

FPIs and market participants have consistently identified India's LTCG, STT, and surcharge structure as factors that reduce post-tax returns and can deter foreign participation, with formal calls to review the capital-gains regime during periods of outflows, as reported by Financial Express.

Budget 2026 STT hike triggered immediate backlash

The steep increase in STT on futures and options announced in February 2026 drew sharp industry criticism and was cited by analysts as a fresh headwind for FPI participation, particularly for derivatives-oriented foreign funds, according to Business Standard.

Cumulative tax burden has risen substantially since 2018

LTCG was raised from 10% to 12.5% in Budget 2024, STCG was hiked to 20%, and STT on options has tripled from 0.05% to 0.15% over three years, creating a progressively heavier tax load on foreign investors that did not exist before 2018.

Contradicting Evidence

FPIs were not continuous net sellers since 2018

The claim of selling "since 2018" is factually incorrect. FPIs were sizeable net buyers in 2019 (approximately ₹1.01 lakh crore), 2020 (approximately ₹1.70 lakh crore), 2021 (approximately ₹25,752 crore), and 2023 (approximately ₹1.71 lakh crore), per NSDL data reported by Times of India and NDTV Profit.

The ₹3.5 lakh crore figure for 2021–2022 is unsupported

In 2021, FPIs were net buyers (roughly ₹25,752 crore to ₹50,089 crore depending on the data source), not sellers. The 2022 equity outflow was approximately ₹1.21 lakh crore. Even combining the most aggressive estimates, the total does not approach ₹3.5 lakh crore for those two years.

2022 outflows were driven largely by global macro factors

The record FPI selling in 2022 coincided with aggressive U.S. Federal Reserve interest rate hikes, a surging dollar, and a global risk-off environment—factors widely cited by analysts as the primary drivers, not domestic tax policy alone.

2023 inflows contradict the policy-exit narrative

If tax policy were the dominant deterrent, it is difficult to explain why FPIs returned with approximately ₹1.71 lakh crore in net equity inflows in 2023—one of the highest totals ever—despite LTCG and STT remaining in force and STT on derivatives having just been hiked in April 2023.

Valuation and relative-return factors are well-documented drivers

The massive 2024-end and 2025 sell-off of approximately ₹1.56–1.66 lakh crore has been widely attributed by analysts to elevated Indian valuations (Nifty trading at significant premiums to emerging-market peers) and a rotation into cheaper markets such as China, which staged a sharp rally, rather than to any new tax measure at that time.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.