On the economic and financial implications of the Middle East War Further to the post below, today’s news is consistent with the view that—judging by their actions—all three warring parties (US, Iran, and Israel) remain in the escalation phase. With each passing day in this phase, the risks of reaching economic and financial tipping points increase. #economy #markets #middleeastwar

Source: Statista

Research Brief

What our analysis found

The Middle East conflict has entered a dangerous new phase of rapid escalation involving all three principal belligerents. On March 13, 2026, the United States bombed military sites on Iran's Kharg Island—the country's primary oil export hub—while President Trump warned that Iran's oil infrastructure could face further strikes and ordered 2,500 Marines and an amphibious assault ship to the region. Days later, on March 17–18, Israel announced it had killed Iran's top security official Ali Larijani, prompting Iran to launch retaliatory missile and drone barrages toward Israel and Gulf states, with interceptions reported in Saudi Arabia and explosions heard in the UAE and Qatar. Two people were killed near Tel Aviv.

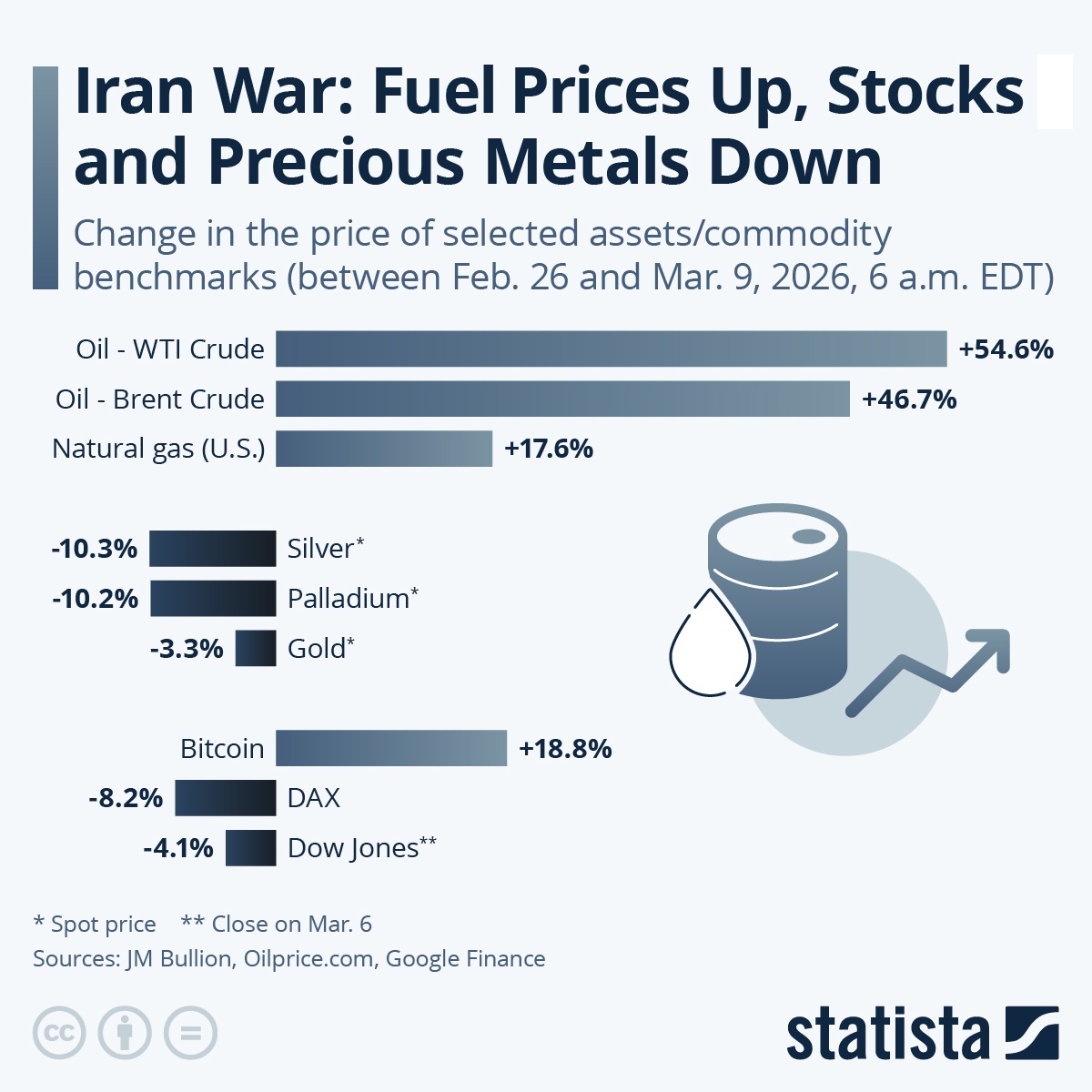

The economic fallout has been swift and severe. Brent crude settled above $103 per barrel on March 17 after touching $106 intraday, while U.S. gasoline prices hit $3.79 per gallon—the highest since 2023—and diesel surged past $5.00 per gallon to $5.04. Shipping through the Strait of Hormuz, which normally carries roughly 20% of the world's oil, collapsed from about 135 vessel passages per day in late February to just 9 vessels on March 2. Only 89 ships crossed the strait between March 1 and 15, compared with the roughly 1,500–2,000 that would transit under normal conditions in the same period. In response, the IEA authorized the largest-ever joint release of emergency oil stocks—up to 400 million barrels—to counter supply disruptions.

Financial markets are flashing stress signals across multiple channels. War-risk insurance premiums for vessels transiting the Gulf surged to 1–1.5% of hull value, up from roughly 0.25% before the conflict, while Hapag-Lloyd imposed war-risk surcharges of $1,500 per TEU on Gulf routes. European natural gas prices rose above €65 per MWh after Qatar halted LNG shipments. In bond markets, U.S. 10-year Treasury yields climbed to approximately 4.13% by March 5, as analysts warned that an energy-driven inflation shock could derail anticipated Federal Reserve rate cuts.

Fact Check

Evidence from both sides

Supporting Evidence

All three parties are actively escalating militarily

The U.S. struck Iran's Kharg Island on March 13 and deployed additional Marines; Israel killed Iran's national security chief Ali Larijani on March 17; Iran launched retaliatory missile and drone barrages on Israel and Gulf states within hours, causing fatalities near Tel Aviv (AP News, multiple reports March 13–18, 2026).

Oil prices have breached critical thresholds

Brent crude surged past $100 per barrel on March 12 (settling at $100.46, up 9.2% in one day) and topped $106 intraday on March 17, representing levels not seen since the 2022 energy crisis and consistent with approaching economic tipping points (AP News).

Consumer fuel costs are spiking sharply

U.S. gasoline hit $3.79 per gallon and diesel exceeded $5.00 per gallon by March 17, raising broad cost-of-living pressures across the economy (AAA data via AP News).

The Strait of Hormuz—a critical global chokepoint—is nearly shut

Traffic collapsed from roughly 135 vessel passages per day in late February to just 9 on March 2; only 89 ships (including 16 oil tankers) transited between March 1 and 15, representing a more than 90% decline in throughput (S&P Global, AP News).

The IEA's historic emergency stock release signals institutional alarm

The coordinated release of up to 400 million barrels—the largest ever—demonstrates that energy authorities view the supply disruption as reaching crisis proportions (IEA, March 11, 2026).

Shipping and insurance costs have surged, compounding supply chain stress

War-risk premiums jumped to 1–1.5% of hull value from 0.25% pre-conflict; Hapag-Lloyd imposed $1,500 per TEU surcharges; tanker day-rates rose approximately 30% to two-year highs (Lloyd's of London via The Guardian, Lloyd's List).

Inflation expectations are being repriced in bond markets

U.S. 10-year Treasury yields rose to roughly 4.13% by March 5, with analysts noting that the energy price shock could force the Federal Reserve to delay or abandon planned rate cuts (Reuters via Sahm Capital).

Contradicting Evidence

The IEA emergency release could blunt the worst supply impacts

The unprecedented authorization to release up to 400 million barrels from strategic reserves represents a powerful countermeasure that could stabilize oil markets and prevent prices from reaching the most extreme tipping-point scenarios, suggesting institutional buffers remain intact (IEA, March 11, 2026).

Strait of Hormuz traffic has not completely ceased

While dramatically reduced, 89 ships—including 16 oil tankers—still transited the strait between March 1 and 15, indicating that the chokepoint has not been fully blockaded and some oil continues to flow, which tempers the most catastrophic supply-disruption forecasts (AP News).

Insurance markets remain functional, if stressed

Lloyd's of London stated that war-risk cover remains available despite sharply higher pricing, suggesting that the market has not reached a point of systemic breakdown where shipping becomes entirely uninsurable—a true financial tipping point (The Guardian).

Oil prices, while elevated, have not reached historic crisis peaks

Brent at $103–106 per barrel is significantly below the inflation-adjusted peaks seen during the 1979 oil crisis or the 2008 spike above $140, suggesting that while stress is mounting, the market has not yet crossed a threshold comparable to past catastrophic disruptions.

All parties may have incentives to de-escalate

The tweet assumes continued escalation, but the very severity of economic consequences—particularly for Iran, whose oil infrastructure is under direct threat, and for the U.S., which faces domestic inflation pressure in a politically sensitive period—could create powerful incentives to pursue diplomatic off-ramps before true tipping points are reached.

Global oil supply is more diversified than in past crises

U.S. shale production, expanded capacity in Guyana, Brazil, and elsewhere, and reduced global dependence on Gulf producers compared to the 1970s and 1980s provide structural buffers that raise the threshold at which supply disruptions become economically catastrophic.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.