The Stock Market Is Underestimating Downside Tail Risks; Goldman Hedge Fund Honcho Warns https://t.co/5JAghFEWUN

Source: Cboe (Chicago Board Options Exchange)

Research Brief

What our analysis found

Goldman Sachs' head of hedge fund coverage, Tony Pasquariello, has warned that "the tails are getting fatter" in equity markets — a pointed message that downside scenario risks are growing faster than prevailing market pricing reflects. The warning comes amid a turbulent stretch for hedge funds: on February 5, 2026, equity long/short managers focused on tech and TMT sectors fell as much as 2.78% in a single day, while multi-strategy funds' equity books dropped 1.9% — their worst session since April 2025, according to a Goldman Sachs prime-brokerage note summarized by Reuters. A second sharp selloff on March 3, 2026 hit Asia-based funds with losses of 3.2% in one day, and the March 7–10 window delivered what Goldman described as one of the worst two-day stretches for hedge fund performance in years.

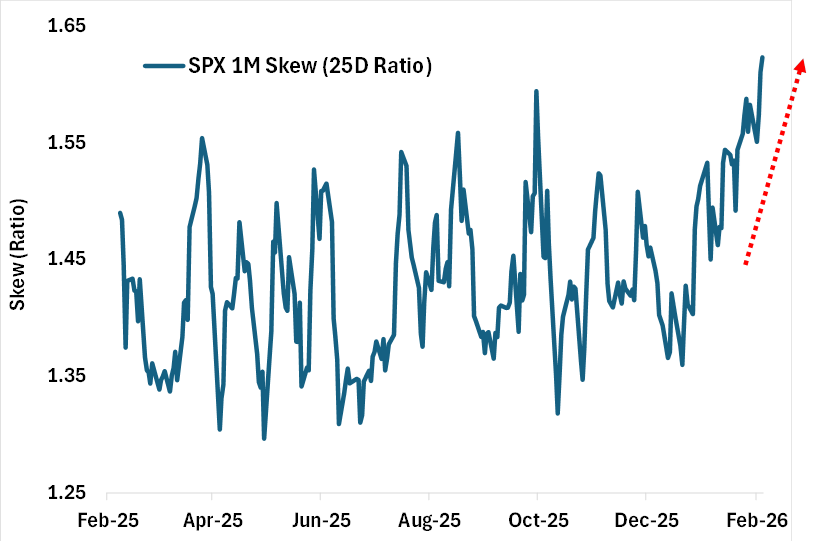

Structural conditions have amplified these shocks. Goldman's 2026 Hedge Fund Industry Outlook noted that gross leverage ended 2025 at the highest level on record, meaning crowded and leveraged positions are vulnerable to rapid unwinding. Meanwhile, options markets have been extraordinarily active: Cboe reported a record index options average daily volume of 6.0 million contracts in February 2026, with zero-days-to-expiration SPX options alone accounting for 3.0 million contracts — 63% of all SPX volume. The Cboe SKEW index, a proxy for tail-risk pricing, rose from roughly 140 in mid-February to 152.44 by March 11, well above its year-ago reading of 132.79.

The debate centers on whether the market has caught up to these risks or remains behind the curve. A January 2026 SocGen quantitative outlook argued that S&P 500 options were assigning a "much lower probability" to a 15–30% drawdown than historical models warranted. Yet by late February, S&P 500 put skew hit a two-year high, and Goldman's own trading desk cautioned that "expectations are no longer cheap," suggesting hedges were becoming expensive — a sign the market may finally be waking up to the threat Pasquariello flagged.

Fact Check

Evidence from both sides

Supporting Evidence

SocGen quant models found downside tails underpriced

A January 16, 2026 SocGen Quant Outlook concluded that S&P 500 options were assigning a "much lower probability" to a 15–30% drawdown over the next year than their quantitative models suggested, directly supporting the claim that markets were underestimating left-tail risks.

Record gross leverage magnifies crash vulnerability

Goldman's 2026 Hedge Fund Industry Outlook reported that hedge fund gross leverage ended 2025 at the highest on record, a structural condition that historically amplifies drawdown severity when shocks occur and is consistent with underappreciated tail risk.

Realized selloff shocks exceeded positioning

The February 5 and March 3–4 selloffs produced single-day hedge fund losses near worst-in-a-year levels — including a 2.78% hit for tech-focused L/S managers and a 3.2% loss for Asia funds — indicating that many funds were not positioned for the magnitude of downside moves that actually materialized.

Goldman Asset Management urged renewed tail-risk hedging

On January 14, 2026, Goldman Sachs Asset Management published a framework emphasizing the "true value" of tail-risk hedging, signaling the firm's own institutional guidance that crash protection deserved more attention than the market was giving it.

Pasquariello's direct warning via client note

Goldman's head of hedge fund coverage told clients that sentiment was "guarded" and that "the tails are getting fatter," explicitly warning that downside scenario risk was rising relative to how markets and hedge funds were positioned.

Contradicting Evidence

Put skew surged to a two-year high

By February 26, 2026, S&P 500 put skew hit its highest level in two years, indicating that options traders were actively paying elevated premiums for downside protection — a sign the market was pricing in tail risk, not ignoring it.

SKEW index climbed well above 2025 levels

The Cboe SKEW index rose from approximately 140 in mid-February to over 152 by March 11, 2026, versus 132.79 a year earlier — historically elevated readings that suggest rising market-implied crash risk premiums rather than complacency.

Goldman's own trading desk said hedges were no longer cheap

A separate Goldman trading-desk summary warned that "expectations are no longer cheap" and advised clients to "hedge the risks everyone knows but few actually own," implying the cost of tail protection had already risen significantly, nuancing the idea that the market was underpricing downside.

Record options volumes reflect intense hedging activity

Cboe's February 2026 record of 6.0 million index options contracts traded per day, with 0DTE SPX options at 3.0 million contracts, demonstrates massive hedging and speculative flows — suggesting market participants were actively engaged with risk management, not ignoring potential drawdowns.

Macro volatility proxies showed caution, not complacency

With the VIX around 17.65 on February 11 and SKEW at approximately 144 on February 12, option markets were signaling a cautious stance even near equity highs, indicating that tail-risk pricing, while debatably insufficient, was not at historically complacent levels.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.