“About once every two years the market falls 10%. Every six years the market’s going to have a 25% decline. That’s all you need to know. You need to know that the market’s going to go down sometimes. If you’re not ready for that, you shouldn’t own stocks.” – Peter Lynch https://t.co/eykNasxLZ4

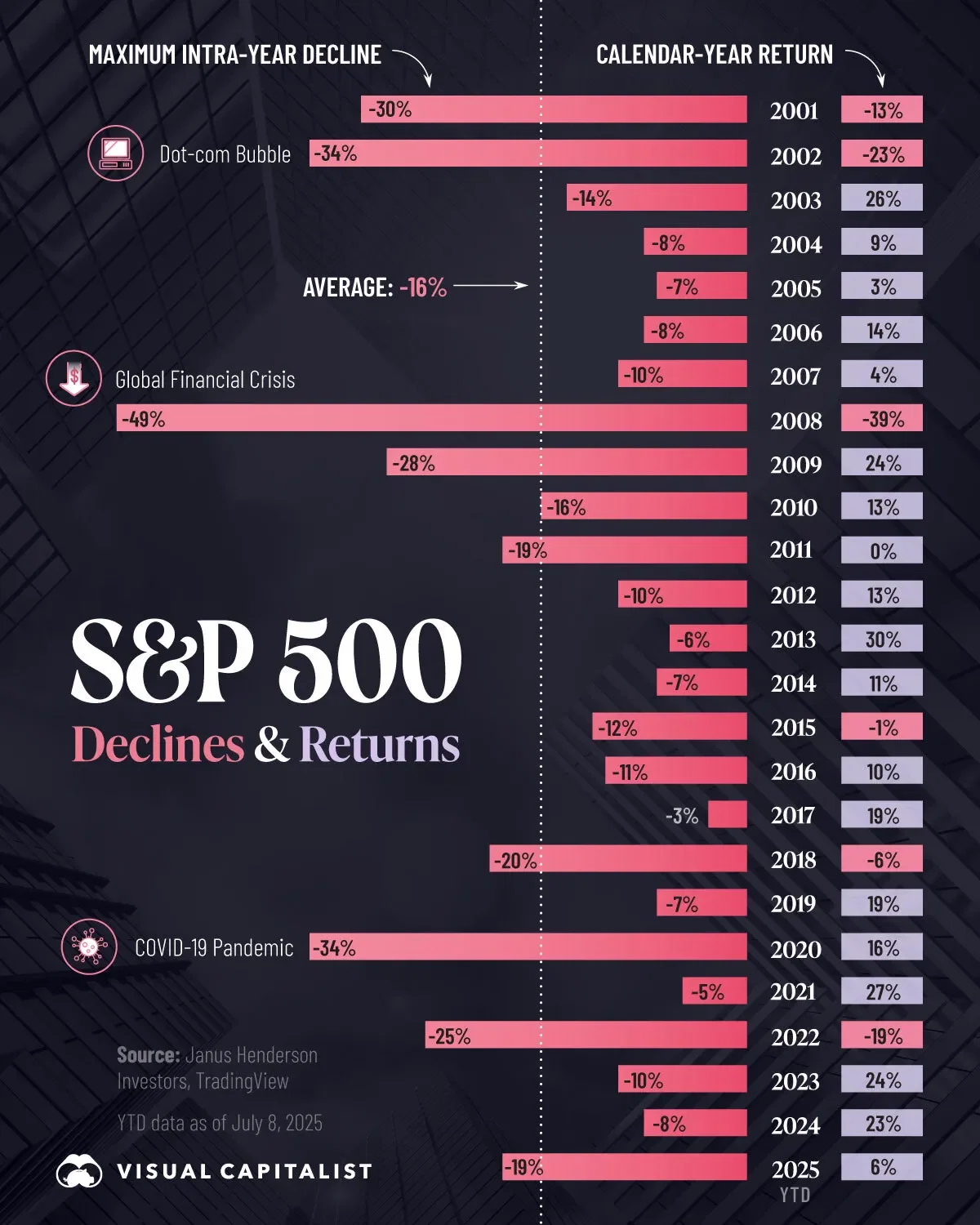

This infographic plots the S&P 500’s maximum intra‑year declines alongside calendar‑year returns (2001–2025), clearly showing frequent ~10% corrections and multiple deeper (~25%+) drawdowns — visually supporting Peter Lynch’s point that market declines of those magnitudes occur regularly and investors should be prepared.

Source: Visual Capitalist (Voronoi)

Research Brief

What our analysis found

The viral tweet attributes a famous investing rule of thumb to legendary Fidelity fund manager Peter Lynch, and the quote is authentic. It originates from Lynch's October 1994 lecture at the National Press Club, where he told the audience that in the 93 years of the 20th century up to that point, the stock market had experienced 50 declines of 10% or more and 15 declines of 25% or more. His simple arithmetic — 50 divided by 93 and 15 divided by 93 — produced the now-iconic heuristics: a 10% correction roughly every two years and a 25% plunge roughly every six years.

Since Lynch delivered those remarks, financial markets have only added to the tally. The dot-com bust of 2000–2002, the Global Financial Crisis of 2007–2009 (which saw the S&P 500 fall approximately 57% peak to trough), the COVID-19 crash of early 2020 (a rapid ~34% decline), the 2022 bear market, and multiple corrections through 2025 have all reinforced the underlying message. Institutional research from firms like Capital Group and State Street, published as recently as 2024–2025, continues to cite broadly similar cadences: 10%+ corrections roughly every one to two years and 20%+ bear markets every five to seven years.

The quote's enduring popularity reflects its power as a psychological anchor for investors. Lynch's core point — that significant drawdowns are a normal, recurring feature of equity markets and that anyone unable to tolerate them should not own stocks — remains widely endorsed by financial advisors and market historians, even as experts caution that the precise numbers depend heavily on methodology, index choice, and time period.

Fact Check

Evidence from both sides

Supporting Evidence

The quote is verified and authentic

Multiple transcripts and video records confirm Peter Lynch made these exact remarks at the National Press Club on October 8, 1994. The 50/15/93 figures appear verbatim in the public record of the lecture (brewbooks.blog transcript, MOI Global posting, C-SPAN references).

Institutional data broadly confirms the 10% correction frequency

Capital Group's client research reports that the S&P 500 has experienced a decline of 10% or more roughly once every 18 months — closely matching Lynch's "about once every two years" heuristic.

Bear-market spacing aligns with the six-year claim

Multiple institutional summaries from Capital Group, State Street, and advisory firms cite 20%+ bear markets as occurring approximately every five to seven years, which is consistent with Lynch's "every six years" estimate for 25%+ declines.

Post-1994 market history has continued the pattern

Major drawdowns since 1994 — the dot-com bust (2000–2002), the Global Financial Crisis (2007–2009, ~57% decline), the COVID crash (2020, ~34%), and the 2022 bear market — demonstrate that large declines have kept recurring at roughly the cadence Lynch described.

The qualitative message is universally endorsed

AP, Kiplinger, and numerous financial advisory sources consistently state that double-digit corrections are routine and that investors should expect them as a normal cost of long-term equity ownership.

Contradicting Evidence

Index choice and methodology significantly alter the count

Lynch's specific tallies depend on which index is used (Dow, S&P 500, Nasdaq), whether intraday or closing prices are measured, and how overlapping declines are counted. Different methods yield frequencies ranging from "once a year" to "once every two years" for 10% drops, meaning his neat ratios are approximations, not precise statistics.

Lynch used a 25% threshold, not the standard 20% bear-market definition

The widely accepted definition of a bear market is a 20% decline, not 25%. Using the lower, conventional threshold increases the count of major drawdowns and changes the average spacing, making Lynch's "every six years" figure appear conservative.

The numbers were a rhetorical heuristic, not a peer-reviewed finding

Lynch's 50 and 15 counts were drawn from a speech aimed at a general audience, not from a formal statistical study. Analysts caution against treating his integers as scientifically precise, as continuing market history since 1994 has added new events that alter the averages.

Averages can mask extreme clustering and long quiet periods

Market corrections and bear markets do not arrive on a neat schedule. Some decades feature multiple severe downturns in quick succession (e.g., 2000–2002 followed by 2007–2009), while other stretches see prolonged calm (e.g., 2009–2018 with relatively few deep corrections), making the "every X years" framing potentially misleading for planning purposes.

The sample period matters greatly

Lynch's data covered roughly 1901–1993. Extending the window back to the 19th century or forward through 2025 changes both the event counts and the average intervals, reminding analysts that frequency estimates are sensitive to the start and end dates chosen.

Report an Issue

Found something wrong with this article? Let us know and we'll look into it.